Ornstein-Uhlenbeck过程维基百科 —— 翻译

原地址:

https://en.wikipedia.org/wiki/Ornstein–Uhlenbeck_process

Ornstein-Uhlenbeck过程

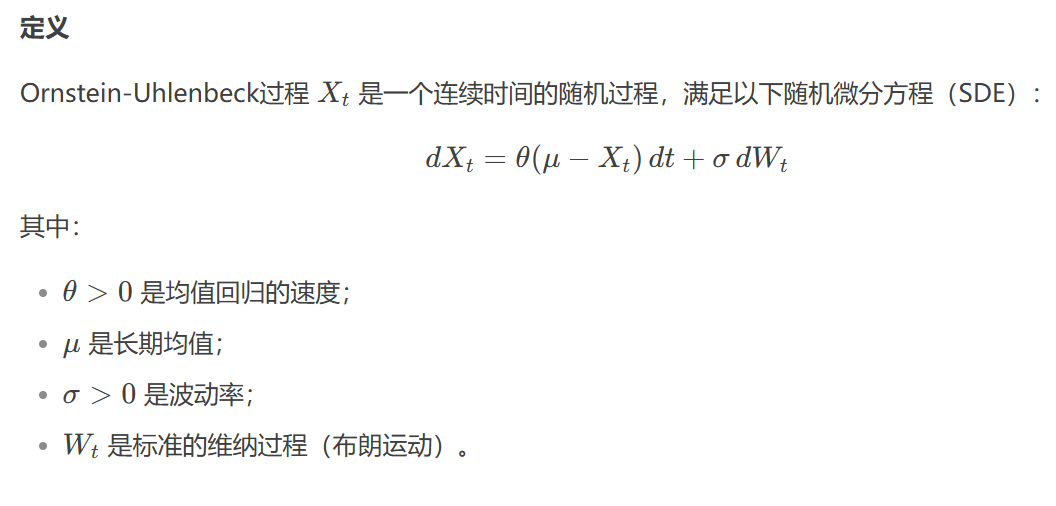

在数学中,Ornstein-Uhlenbeck过程(以Leonard Ornstein和George Eugene Uhlenbeck命名)是一个随机过程,用于描述受到随机扰动的系统在趋向于某个平衡状态时的行为。它是一个平稳高斯马尔可夫过程,广泛应用于物理学、金融数学和其他领域。

历史

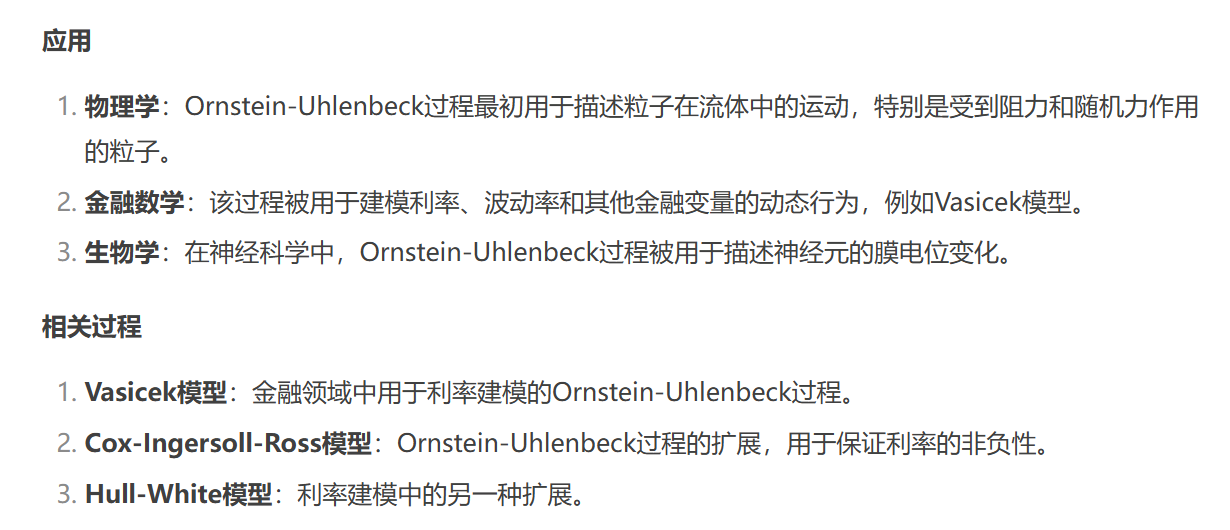

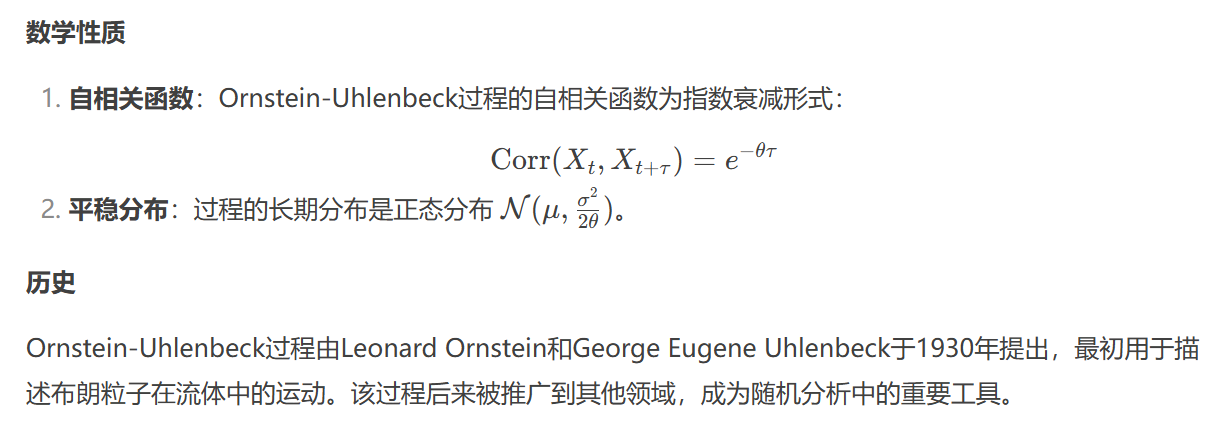

Ornstein-Uhlenbeck过程由Leonard Ornstein和George Eugene Uhlenbeck于1930年提出,最初用于描述布朗粒子在流体中的运动。该过程后来被推广到其他领域,成为随机分析中的重要工具。

参考文献

Ornstein, L. S., & Uhlenbeck, G. E. (1930). "On the theory of the Brownian motion". Physical Review.

Vasicek, O. (1977). "An equilibrium characterization of the term structure". Journal of Financial Economics.

Cox, J. C., Ingersoll, J. E., & Ross, S. A. (1985). "A theory of the term structure of interest rates". Econometrica.

本博客是博主个人学习时的一些记录,不保证是为原创,个别文章加入了转载的源地址,还有个别文章是汇总网上多份资料所成,在这之中也必有疏漏未加标注处,如有侵权请与博主联系。

如果未特殊标注则为原创,遵循 CC 4.0 BY-SA 版权协议。

posted on 2025-03-01 12:58 Angry_Panda 阅读(121) 评论(0) 收藏 举报

浙公网安备 33010602011771号

浙公网安备 33010602011771号