机器学习(Andrew Ng)作业代码(Exercise 1~2)

Programming Exercise 1: Linear Regression

单变量线性回归

warmUpExercise

要求:输出5阶单位阵

直接使用eye(5,5)即可

function A = warmUpExercise()

%WARMUPEXERCISE Example function in octave

% A = WARMUPEXERCISE() is an example function that returns the 5x5 identity matrix

A = [];

% ============= YOUR CODE HERE ==============

% Instructions: Return the 5x5 identity matrix

% In octave, we return values by defining which variables

% represent the return values (at the top of the file)

% and then set them accordingly.

A=eye(5,5);

% ===========================================

end

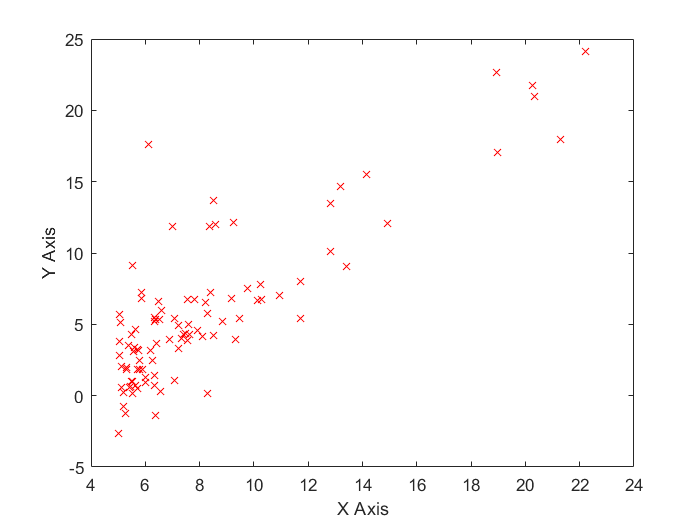

plotData

要求:读入若干组数据(x,y),将它们绘制成散点图

使用MATLAB的plot()命令即可

function plotData(x, y)

%PLOTDATA Plots the data points x and y into a new figure

% PLOTDATA(x,y) plots the data points and gives the figure axes labels of

% population and profit.

% ====================== YOUR CODE HERE ======================

% Instructions: Plot the training data into a figure using the

% "figure" and "plot" commands. Set the axes labels using

% the "xlabel" and "ylabel" commands. Assume the

% population and revenue data have been passed in

% as the x and y arguments of this function.

%

% Hint: You can use the 'rx' option with plot to have the markers

% appear as red crosses. Furthermore, you can make the

% markers larger by using plot(..., 'rx', 'MarkerSize', 10);

figure; % open a new figure window

data=load('ex1data1.txt');

[n,m]=size(data);

xdata=data(:,1);

ydata=data(:,2);

for i=1:n

plot(xdata,ydata,'rx');

end

xlabel('X Axis');

ylabel('Y Axis');

% ============================================================

end

输出结果:

computeCost

要求:读入\(m\)组数据(X,y),计算用\(y=\theta^T X(\theta=(\theta_0,\theta_1)^T,X=(1,x^{(i)})^T)\)拟合这组数据的均方误差\(J(\theta)\)

function J = computeCost(X, y, theta)

%传入:X为m*2矩阵,每一行第一列为1,第二个为X值,y为m维行向量,theta为二维列向量

%COMPUTECOST Compute cost for linear regression

% J = COMPUTECOST(X, y, theta) computes the cost of using theta as the

% parameter for linear regression to fit the data points in X and y

% Initialize some useful values

m = length(y); % number of training examples

% You need to return the following variables correctly

J = 0;

% ====================== YOUR CODE HERE ======================

% Instructions: Compute the cost of a particular choice of theta

% You should set J to the cost.

for i=1:m

J=J+(theta'*X(i,:)'-y(i))^2;

end

J=J/(2*m);

% =========================================================================

end

gradientDescent

要求:给出m组数据\((x^{(i)},y^{(i)})\),学习率\(\alpha\),梯度下降法迭代num_iters次后返回最终的参数\(\theta\)和每次迭代后的均方误差损失J_history

公式推导:

梯度下降过程中,每次迭代同时更新\(\theta_0,\theta_1\):

function [theta, J_history] = gradientDescent(X, y, theta, alpha, num_iters)

%GRADIENTDESCENT Performs gradient descent to learn theta

% theta = GRADIENTDESENT(X, y, theta, alpha, num_iters) updates theta by

% taking num_iters gradient steps with learning rate alpha

% Initialize some useful values

m = length(y); % number of training examples

J_history = zeros(num_iters, 1);

for iter = 1:num_iters

% ====================== YOUR CODE HERE ======================

% Instructions: Perform a single gradient step on the parameter vector

% theta.

%

% Hint: While debugging, it can be useful to print out the values

% of the cost function (computeCost) and gradient here.

%

dJ_dtheta0=0;

dJ_dtheta1=0;

for i=1:m

dJ_dtheta0=dJ_dtheta0+(theta'*X(i,:)'-y(i));

dJ_dtheta1=dJ_dtheta1+(theta'*X(i,:)'-y(i))*X(i,2);

end

dJ_dtheta0=dJ_dtheta0/m;

dJ_dtheta1=dJ_dtheta1/m;

theta=theta-alpha*([dJ_dtheta0,dJ_dtheta1])';

% ============================================================

% Save the cost J in every iteration

J_history(iter) = computeCost(X, y, theta)

end

end

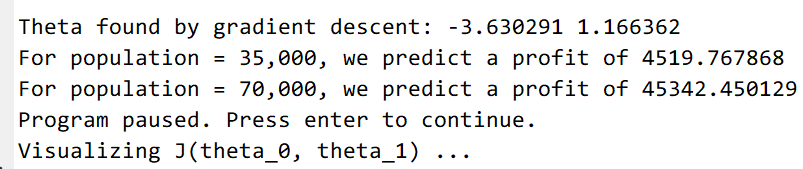

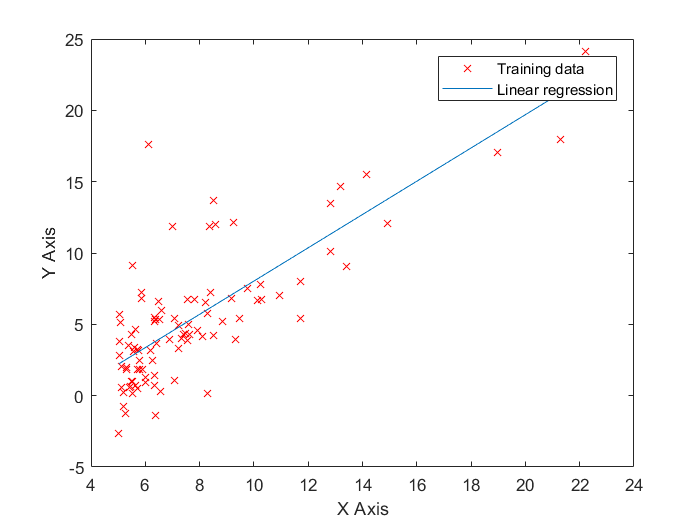

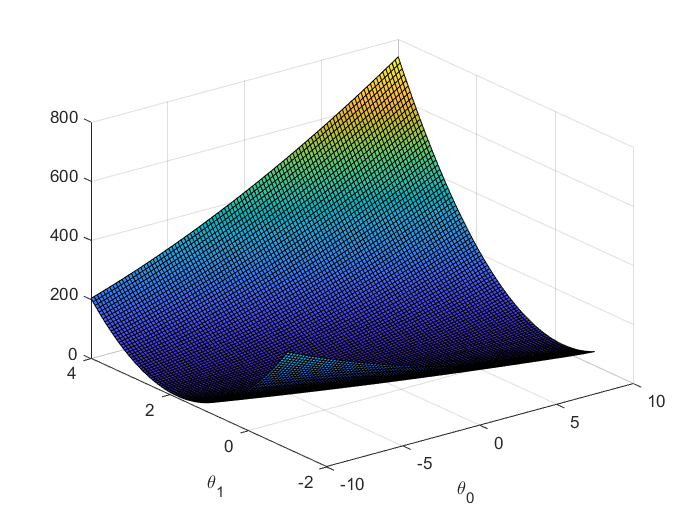

最终运行结果

Fig1.梯度下降法线性回归拟合出的直线

Fig2.\(J(\theta)\)的曲面图像

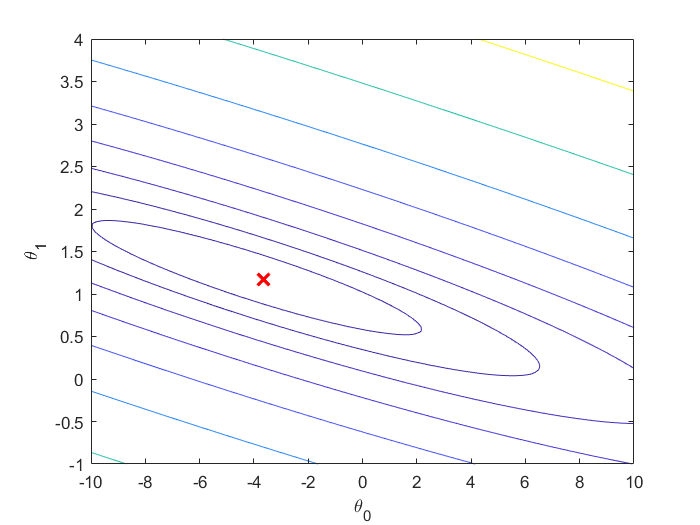

Fig3.\(J(\theta)\)的等高线图,红叉代表了\(J(\theta)\)最小处的点

多变量线性回归

featureNormalize

要求:给出m组输入数据的特征(这里特征维数为2),即m行2列矩阵X,将输入数据Z-score归一化到区间[-1,1]。注意,这时还没有给X添加一列1

Z-score归一化方法:

对于第i维特征,计算出m组数据该特征的平均值\(\mu\)和标准差\(\sigma\),则

归一化后每一维特征平均值为0,标准差为1

function [X_norm, mu, sigma] = featureNormalize(X)

%FEATURENORMALIZE Normalizes the features in X

% FEATURENORMALIZE(X) returns a normalized version of X where

% the mean value of each feature is 0 and the standard deviation

% is 1. This is often a good preprocessing step to do when

% working with learning algorithms.

% You need to set these values correctly

X_norm = X;

mu = zeros(1, size(X, 2));

sigma = zeros(1, size(X, 2));

% ====================== YOUR CODE HERE ======================

% Instructions: First, for each feature dimension, compute the mean

% of the feature and subtract it from the dataset,

% storing the mean value in mu. Next, compute the

% standard deviation of each feature and divide

% each feature by it's standard deviation, storing

% the standard deviation in sigma.

%

% Note that X is a matrix where each column is a

% feature and each row is an example. You need

% to perform the normalization separately for

% each feature.

%

% Hint: You might find the 'mean' and 'std' functions useful.

%

mu(1,1)=mean(X(:,1));

mu(1,2)=mean(X(:,2));

sigma(1,1)=std(X(:,1));

sigma(1,2)=std(X(:,2));

X_norm(:,1)=(X_norm(:,1)-mu(1,1))/sigma(1,1);

X_norm(:,2)=(X_norm(:,2)-mu(1,2))/sigma(1,2);

% ============================================================

end

computeCostMulti

要求:给出m组输入数据(m*3矩阵X,每一行第一列为1)和真实输出y,计算用\(y=\theta^TX^{(i)T}\)拟合这些数据的均方误差\(J(\theta)\)

function J = computeCostMulti(X, y, theta)

%COMPUTECOSTMULTI Compute cost for linear regression with multiple variables

% J = COMPUTECOSTMULTI(X, y, theta) computes the cost of using theta as the

% parameter for linear regression to fit the data points in X and y

% Initialize some useful values

m = length(y); % number of training examples

% You need to return the following variables correctly

J = 0;

% ====================== YOUR CODE HERE ======================

% Instructions: Compute the cost of a particular choice of theta

% You should set J to the cost.

for i=1:m

J=J+(theta'*X(i)'-y(i))^2;

end

J=J/(2*m);

% =========================================================================

end

gradientDescentMulti

要求:给出m组数据\((x^{(i)},y^{(i)})\),学习率\(\alpha\),梯度下降法迭代num_iters次后返回最终的参数\(\theta\)和每次迭代后的均方误差损失J_history

注意,这里每个输入数据的第一维特征都是1(后来补上的)

公式推导:

对于第t个参数\(\theta_t\),其更新公式为:

function [theta, J_history] = gradientDescentMulti(X, y, theta, alpha, num_iters)

%GRADIENTDESCENTMULTI Performs gradient descent to learn theta

% theta = GRADIENTDESCENTMULTI(x, y, theta, alpha, num_iters) updates theta by

% taking num_iters gradient steps with learning rate alpha

% Initialize some useful values

m = length(y); % number of training examples

J_history = zeros(num_iters, 1);

for iter = 1:num_iters

% ====================== YOUR CODE HERE ======================

% Instructions: Perform a single gradient step on the parameter vector

% theta.

%

% Hint: While debugging, it can be useful to print out the values

% of the cost function (computeCostMulti) and gradient here.

%

paramsize=length(theta);

dJ_dtheta=zeros(paramsize,1);

for i=1:paramsize

for j=1:m

dJ_dtheta(i,1)=dJ_dtheta(i,1)+(theta'*X(j,:)'-y(j))*X(j,i);

end

end

for i=1:paramsize

dJ_dtheta(i,1)=dJ_dtheta(i,1)/m;

theta(i)=theta(i)-alpha*dJ_dtheta(i);

end

% ============================================================

% Save the cost J in every iteration

J_history(iter) = computeCostMulti(X, y, theta);

end

end

最终测试结果

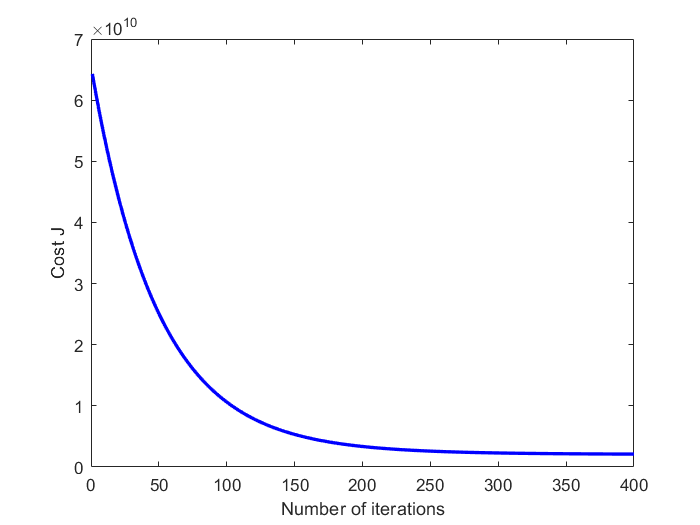

Fig1.收敛曲线

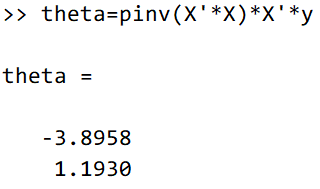

最小二乘法(投影法)求\(\theta\)

对于单变量的线性回归问题,

结果与梯度下降法近似。

Programming Exercise 2: Logistic Regression

Logistic回归二分类

plotData

function plotData(X, y)

%PLOTDATA Plots the data points X and y into a new figure

% PLOTDATA(x,y) plots the data points with + for the positive examples

% and o for the negative examples. X is assumed to be a Mx2 matrix.

% Create New Figure

figure; hold on;

% ====================== YOUR CODE HERE ======================

% Instructions: Plot the positive and negative examples on a

% 2D plot, using the option 'k+' for the positive

% examples and 'ko' for the negative examples.

%

m=size(X,1);

pos=find(y==1);

neg=find(y==0);

plot(X(pos,1),X(pos,2),'+','LineWidth', 2,'MarkerSize', 7);

plot(X(neg,1),X(neg,2),'o', 'MarkerFaceColor', 'y','MarkerSize', 7);

% =========================================================================

hold off;

end

sigmoid

Sigmoid函数:

function g = sigmoid(z)

%SIGMOID Compute sigmoid functoon

% J = SIGMOID(z) computes the sigmoid of z.

% You need to return the following variables correctly

g = zeros(size(z));

% ====================== YOUR CODE HERE ======================

% Instructions: Compute the sigmoid of each value of z (z can be a matrix,

% vector or scalar).

g=1/(1+exp(-z));

% =============================================================

end

costFunction

Logistic回归采用交叉熵误差函数:

梯度下降公式推导:

function [J, grad] = costFunction(theta, X, y)

%COSTFUNCTION Compute cost and gradient for logistic regression

% J = COSTFUNCTION(theta, X, y) computes the cost of using theta as the

% parameter for logistic regression and the gradient of the cost

% w.r.t. to the parameters.

% Initialize some useful values

m = length(y); % number of training examples

% You need to return the following variables correctly

J = 0;

grad = zeros(size(theta));

% ====================== YOUR CODE HERE ======================

% Instructions: Compute the cost of a particular choice of theta.

% You should set J to the cost.

% Compute the partial derivatives and set grad to the partial

% derivatives of the cost w.r.t. each parameter in theta

%

% Note: grad should have the same dimensions as theta

%

for i=1:m

J=J+(-y(i)*log(sigmoid(theta'*X(i,:)'))-(1-y(i))*log(1-sigmoid(theta'*X(i,:)')));

end

J=J/m;

for t=1:size(theta)

for i=1:m

grad(t)=grad(t)+(sigmoid(theta'*X(i,:)')-y(i))*X(i,t);

end

grad(t)=grad(t)/m;

end

% =============================================================

end

predict

function p = predict(theta, X)

%PREDICT Predict whether the label is 0 or 1 using learned logistic

%regression parameters theta

% p = PREDICT(theta, X) computes the predictions for X using a

% threshold at 0.5 (i.e., if sigmoid(theta'*x) >= 0.5, predict 1)

m = size(X, 1); % Number of training examples

% You need to return the following variables correctly

p = zeros(m, 1);

% ====================== YOUR CODE HERE ======================

% Instructions: Complete the following code to make predictions using

% your learned logistic regression parameters.

% You should set p to a vector of 0's and 1's

%

for i=1:m

tmp=theta'*X(i,:)';

if(tmp>=0)

p(i)=1;

else

p(i)=0;

end

end

% =========================================================================

end

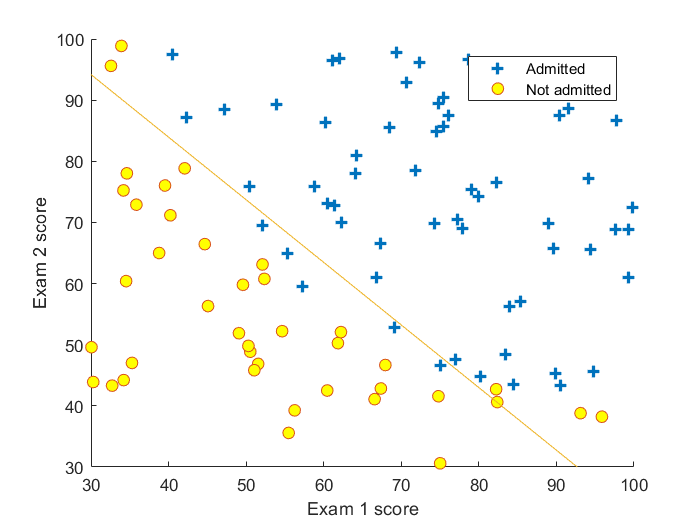

最终测试结果

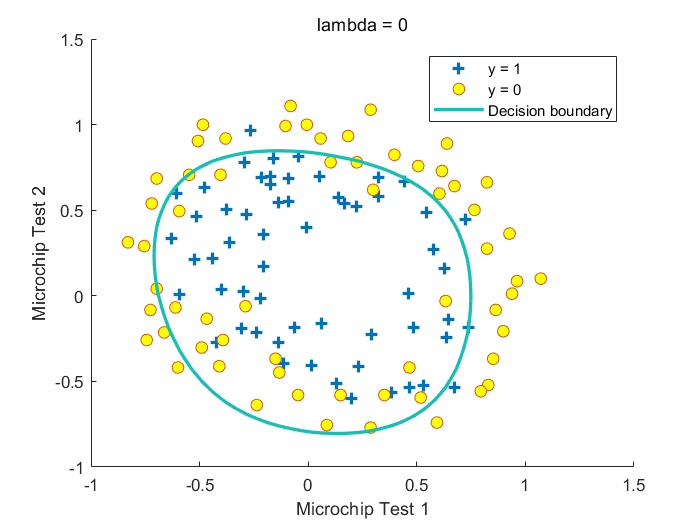

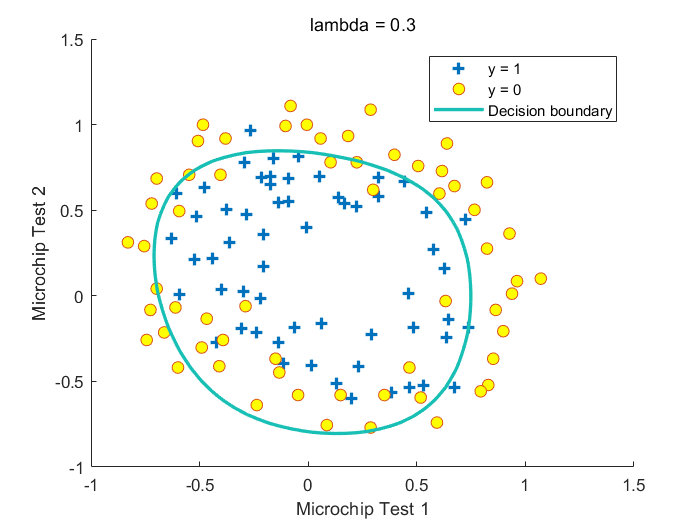

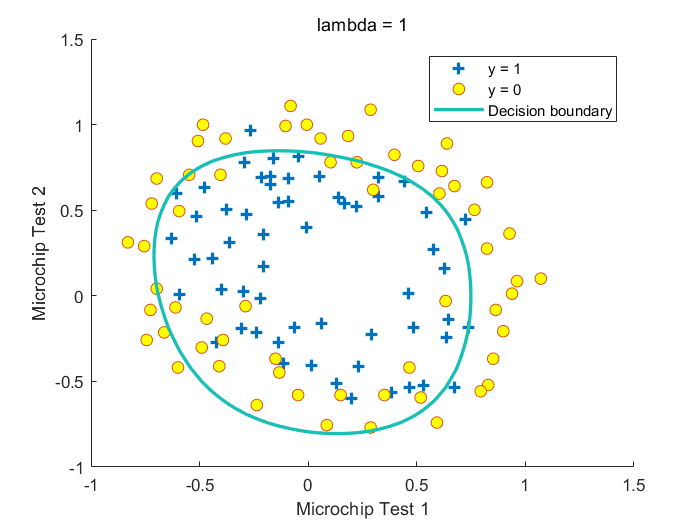

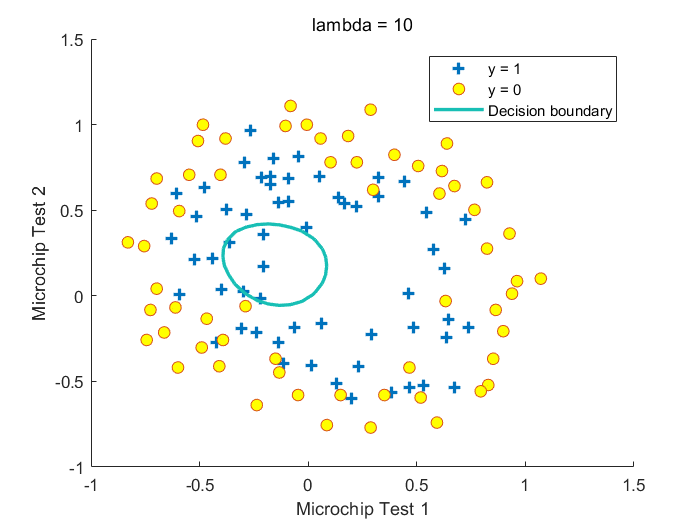

带正则化的Logistic回归二分类

costFunctionReg

带正则化的Logistic回归中,损失函数加入了正则化项

其中\(\lambda\)为惩罚参数,\(\lambda\)越大,\(\theta_1\cdots \theta_n\)越小,\(h_\theta(X)\)越接近\(Sigmoid(\theta_0)\),越不容易过拟合,倾向于欠拟合。注意这里没有把\(\theta_0\)加入正则化项中

梯度下降公式推导:

function [J, grad] = costFunctionReg(theta, X, y, lambda)

%COSTFUNCTIONREG Compute cost and gradient for logistic regression with regularization

% J = COSTFUNCTIONREG(theta, X, y, lambda) computes the cost of using

% theta as the parameter for regularized logistic regression and the

% gradient of the cost w.r.t. to the parameters.

% Initialize some useful values

m = length(y); % number of training examples

% You need to return the following variables correctly

J = 0;

grad = zeros(size(theta));

% ====================== YOUR CODE HERE ======================

% Instructions: Compute the cost of a particular choice of theta.

% You should set J to the cost.

% Compute the partial derivatives and set grad to the partial

% derivatives of the cost w.r.t. each parameter in theta

for i=1:m

tmp=sigmoid(theta'*X(i,:)');

J=J+(-y(i)*log(tmp)-(1-y(i))*log(1-tmp));

end

J=J/m;

regsum=0;

for i=2:size(theta)

regsum=regsum+theta(i)*theta(i);

end

regsum=regsum*lambda/(2*m);

J=J+regsum;

for i=1:m

grad(1)=grad(1)+(sigmoid(theta'*X(i,:)')-y(i))*X(i,1);

end

grad(1)=grad(1)/m;

for t=2:size(theta)

for i=1:m

grad(t)=grad(t)+(sigmoid(theta'*X(i,:)')-y(i))*X(i,t);

end

grad(t)=grad(t)+lambda*theta(t)/m;

end

% =============================================================

end

最终测试结果

Fig.不同\(\lambda\)取值下获得的决策边界

浙公网安备 33010602011771号

浙公网安备 33010602011771号