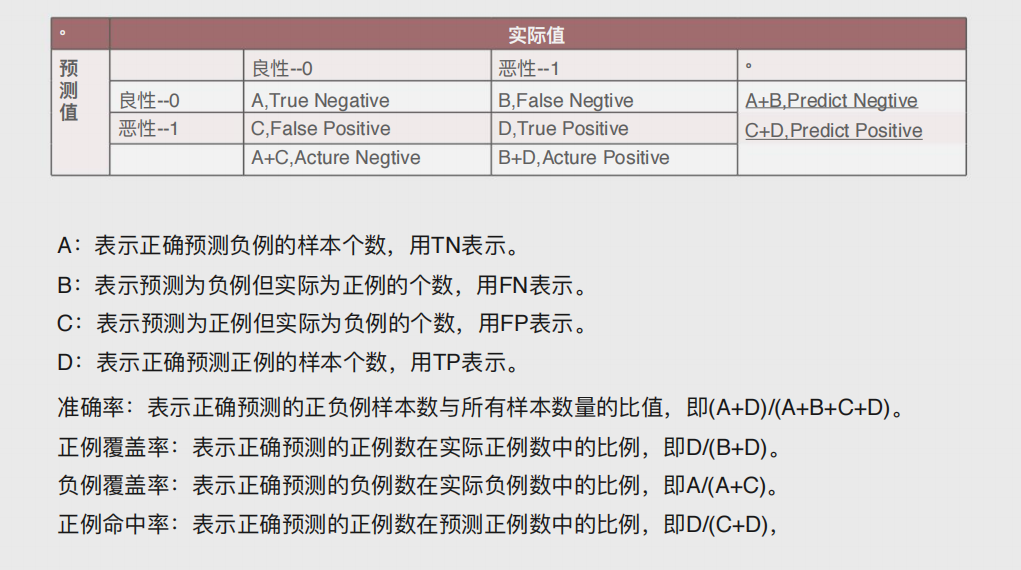

算法模型补充

-

模型的假设检验(F与T)

-

岭回归与Lasso回归

-

Logistic回归模型

-

决策树与随机森林

-

K近邻模型

详情

-

模型的假设检验(F与T)

F检验

F检验:提出原假设(不合理)和备择假设(合理),之后计算实际值与理论值,通过比较两者判断模型是否合理。

计算实际值

# 需要导入相关模块 import numpy as np import pandas as pd from sklearn import model_selection import statsmodels.api as sm # 读取数据 pt = pd.read_excel(r'Predict to Profit.xlsx') # 拆分训练集与测试集 train,test = model_selection.train_test_split(pt,test_size=0.2,random_state=1234) # 建立模型 pModel = sm.formula.ols('Profit~RD_Spend+Administration+Marketing_Spend+C(State)',data=train).fit() # 计算建模中因变量的均值 yMean = train.Profit.mean() # 115525.98769230771 # 统计变量个数与观测个数 p = pModel.df_model # 5 n = train.shape[0] # 39 # 计算回归离差平方和 52067443965.96364 RSS = np.sum((pModel.fittedvalues-yMean)**2) # 计算误差平方和 1967765724.576366 ESS = np.sum(pModel.resid**2) # 计算F实际值 F = (RSS/p)/(ESS/(n-p-1)) print('F统计量的值: ', F)

计算理论值

# 导⼊模块 from scipy.stats import f # 计算F理论值 FT = f.ppf(q=0.95,dfn = p,dfd = n-p-1) print('F理论值为: ', FT)

结论:计算出来的F统计量值174.64远远⼤于F分布的理论值2.50 所以应当拒绝原假设(先假设模型不合理),即多元线性回归模型是显著的,偏回归系数不全为0。

T检验

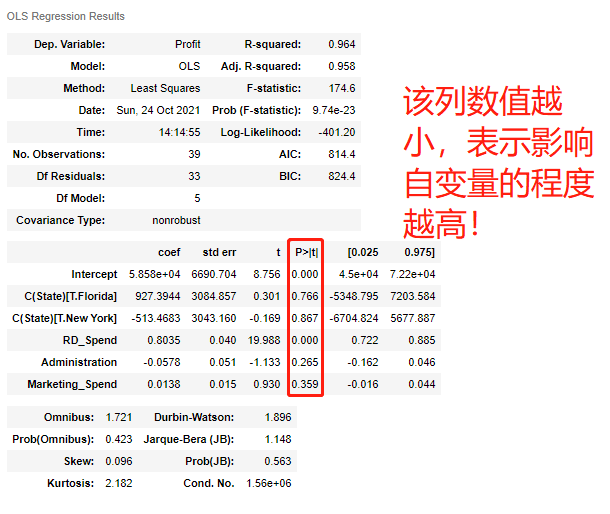

"""T检验更加侧重于检验模型的各个参数是否合理""" model.summary() # 结果中P>|t|的绝对值越小对自变量的影响越大

线性回归模型的短板

虽然有上述方法来检验模型以及参数的合理性,线性回归模型依旧存在不适用的场合。

1、自变量个数大于样本量。

2、自变量直接存在多重共线性(值高度相关)。

为了解决上述问题,需要使用岭回归模型与Lasso回归模型。

-

岭回归与Lasso回归

岭回归模型

在线性回归模型的基础之上添加一个l2惩罚项(也称平方项、正则项)。

线性回归模型:J(β)=∑(y−Xβ)^2

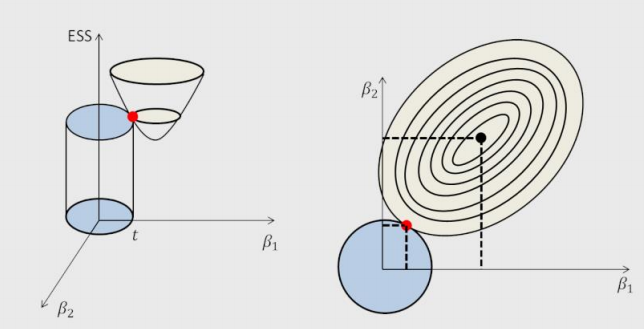

岭回归模型:J(β)=∑(y−Xβ)^2+∑λβ^2

该模型最终转变成求解圆柱体与椭圆抛物线的交点问题,始终保留建模时的所有变量,无法降低模型的复杂度。

岭回归交叉验证的参数

RidgeCV(alphas=(0.1, 1.0, 10.0), fit_intercept=True, normalize=False, scoring=None, cv=None) # 参数 alphas:⽤于指定多个lambda值的元组或数组对象,默认该参数包含0.1、1和10三种值。 fit_intercept:bool类型参数,是否需要拟合截距项,默认为True。 normalize:bool类型参数,建模时是否需要对数据集做标准化处理,默认为False。 scoring:指定⽤于评估模型的度量⽅法。 cv:指定交叉验证的重数。

岭回归模型案例

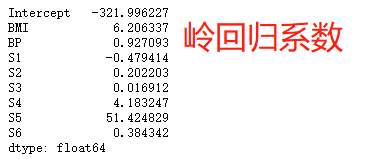

'''求最准确的Lamda值''' # 导入模块 from sklearn.linear_model import Ridge,RidgeCV # 读取糖尿病数据集 diabetes = pd.read_excel(r'diabetes.xlsx') # 构造自变量(剔除患者性别、年龄和因变量) predictors = diabetes.columns[2:-1] # 将数据集拆分为训练集和测试集 X_train, X_test, y_train, y_test = model_selection.train_test_split(diabetes[predictors], diabetes['Y'],test_size = 0.2, random_state = 1234) # 构造不同的Lamda值 Lambdas=np.logspace(-5,2,200) # 设置交叉验证的参数,对于每一个Lambda值,都执行10重交叉验证 ridge_cv = RidgeCV(alphas = Lambdas, normalize=True, scoring='neg_mean_squared_error', cv = 10) # 模型拟合 ridge_cv.fit(X_train, y_train) # 返回最佳的lambda值 ridge_best_Lambda = ridge_cv.alpha_ ridge_best_Lambda # 0.014649713983072863 '''基于最准确的Lamda值建模''' # 导入第三方包中的函数 from sklearn.metrics import mean_squared_error # 基于最佳的Lambda值建模 ridge = Ridge(alpha = ridge_best_Lambda, normalize=True) ridge.fit(X_train, y_train) # 返回岭回归系数 pd.Series(index = ['Intercept'] + X_train.columns.tolist(),data = [ridge.intercept_] + ridge.coef_.tolist()) # 预测 ridge_predict = ridge.predict(X_test) # 预测效果验证:均方根误差 RMSE = np.sqrt(mean_squared_error(y_test,ridge_predict)) RMSE # 53.119117887535204

Lasso回归模型

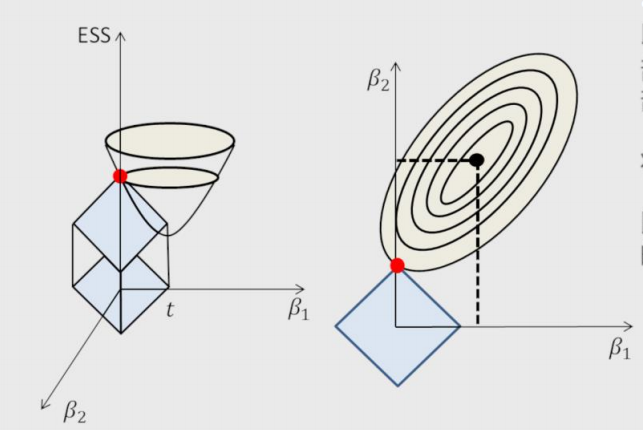

在线性回归模型的基础之上添加一个l1惩罚项(也称正则项)。

Lasso回归模型:J(β)=∑(y−Xβ)^2+∑λ|β| 该模型最终转变成求解正方体与椭圆抛物线的交点问题,相较于岭回归降低了模型的复杂度。

Lasso回归交叉验证的参数

LassoCV(alphas=None, fit_intercept=True, normalize=False,max_iter=1000, tol=0.0001) # 参数 alphas:指定具体的Lambda值列表⽤于模型的运算 fit_intercept:bool类型参数,是否需要拟合截距项,默认为True normalize:bool类型参数,建模时是否需要对数据集做标准化处理,默认为False max_iter:指定模型最⼤的迭代次数,默认为1000次

Lasso回归模型案例

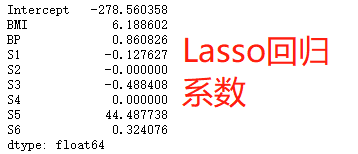

'''求最准确的Lamda值''' # 导入第三方模块中的函数 from sklearn.linear_model import Lasso,LassoCV # LASSO回归模型的交叉验证 lasso_cv = LassoCV(alphas = Lambdas, normalize=True, cv = 10, max_iter=10000) lasso_cv.fit(X_train, y_train) # 输出最佳的lambda值 lasso_best_alpha = lasso_cv.alpha_ lasso_best_alpha # 0.06294988990221888 '''基于最准确的Lamda值建模''' # 基于最佳的lambda值建模 lasso = Lasso(alpha = lasso_best_alpha, normalize=True, max_iter=10000) lasso.fit(X_train, y_train) # 返回LASSO回归的系数 xs=pd.Series(index = ['Intercept'] + X_train.columns.tolist(),data = [lasso.intercept_] + lasso.coef_.tolist()) xs # 预测 lasso_predict = lasso.predict(X_test) # 预测效果验证 RMSE = np.sqrt(mean_squared_error(y_test,lasso_predict)) RMSE # 53.06143725822573

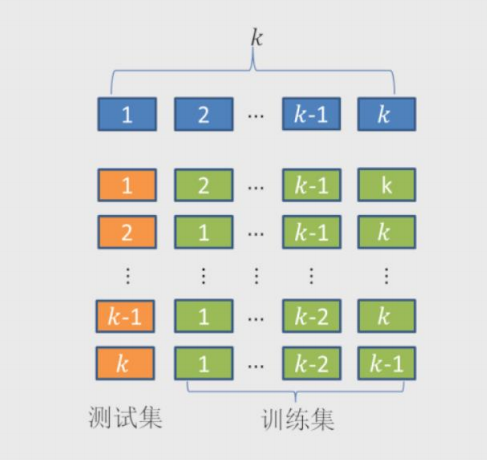

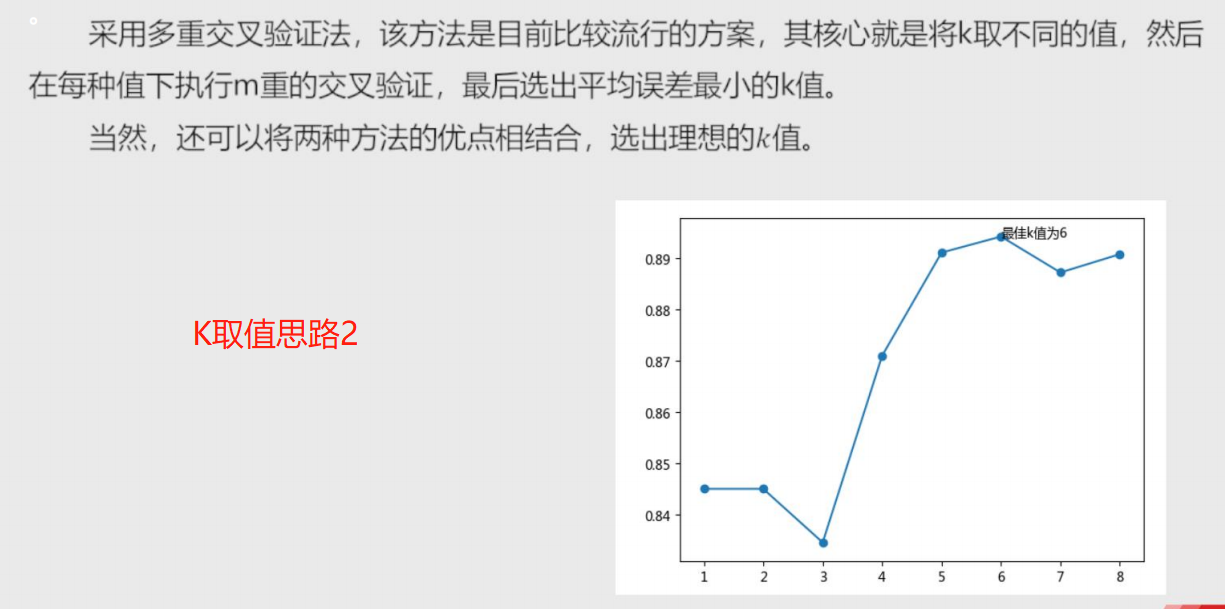

交叉验证的思想

1.将数据集拆分成k个样本量相当的数据组,组件无重叠样本。

2.从k组数据中挑选k-1组用于构建模型,剩下一组用于测试。

3.以此类推,会获得k种训练集和测试集,每一个数据组都将参与构建以及测试。

4.从中选择准确度最高的模型。

-

Logistic回归模型

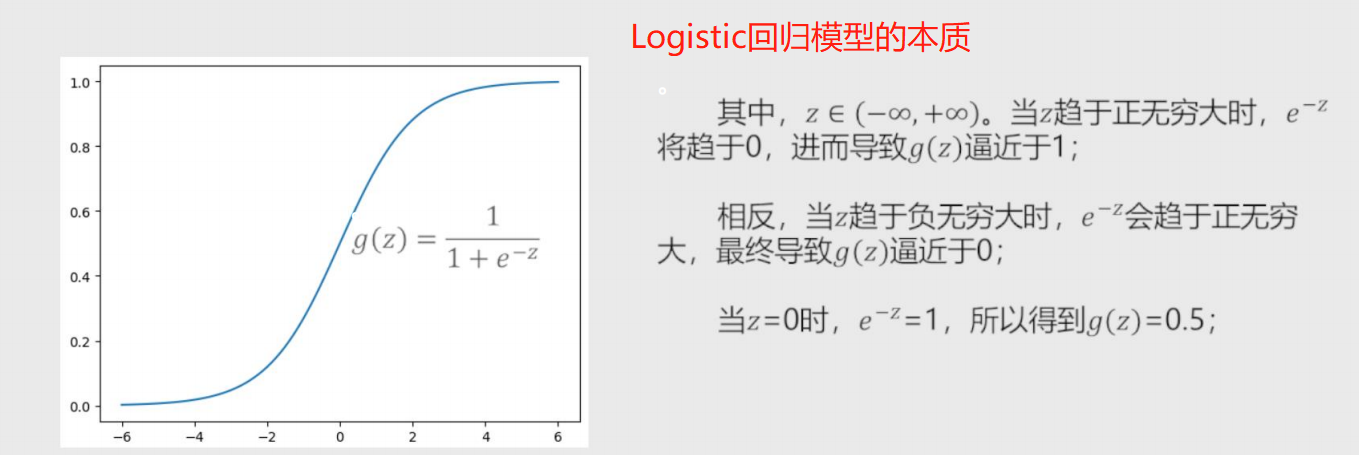

将线性回归模型的公式做Logit变换即为Logistic回归模型

原本的线性回归模型:y = β + β1x1 + β2x2 + ... + βpxp

Logit编号:g(y) = 1/(1+e^(-y)) = hβ(x)

hβ(x)称为Logistic回归模型,将预测问题变成了0到1之间的概率问题。

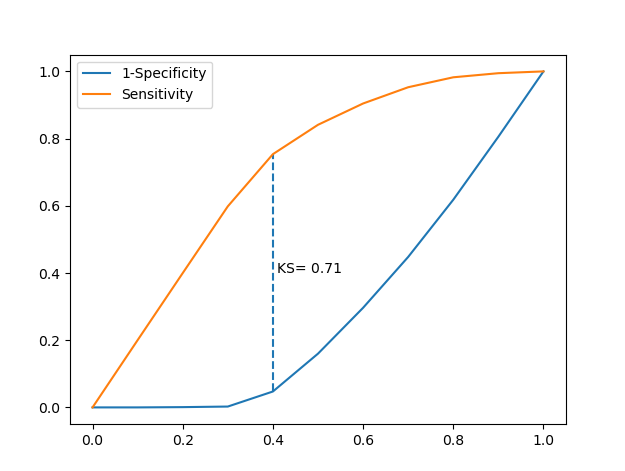

自定义绘制ks曲线的函数

# 导入第三方模块 import pandas as pd import numpy as np import matplotlib.pyplot as plt from sklearn import model_selection from sklearn import linear_model # 自定义绘制ks曲线的函数 def plot_ks(y_test, y_score, positive_flag): # 对y_test重新设置索引 y_test.index = np.arange(len(y_test)) # 构建目标数据集 target_data = pd.DataFrame({'y_test':y_test, 'y_score':y_score}) # 按y_score降序排列 target_data.sort_values(by = 'y_score', ascending = False, inplace = True) # 自定义分位点 cuts = np.arange(0.1,1,0.1) # 计算各分位点对应的Score值 index = len(target_data.y_score)*cuts scores = np.array(target_data.y_score)[index.astype('int')] # 根据不同的Score值,计算Sensitivity和Specificity Sensitivity = [] Specificity = [] for score in scores: # 正例覆盖样本数量与实际正例样本量 positive_recall = target_data.loc[(target_data.y_test == positive_flag) & (target_data.y_score>score),:].shape[0] positive = sum(target_data.y_test == positive_flag) # 负例覆盖样本数量与实际负例样本量 negative_recall = target_data.loc[(target_data.y_test != positive_flag) & (target_data.y_score<=score),:].shape[0] negative = sum(target_data.y_test != positive_flag) Sensitivity.append(positive_recall/positive) Specificity.append(negative_recall/negative) # 构建绘图数据 plot_data = pd.DataFrame({'cuts':cuts,'y1':1-np.array(Specificity),'y2':np.array(Sensitivity), 'ks':np.array(Sensitivity)-(1-np.array(Specificity))}) # 寻找Sensitivity和1-Specificity之差的最大值索引 max_ks_index = np.argmax(plot_data.ks) plt.plot([0]+cuts.tolist()+[1], [0]+plot_data.y1.tolist()+[1], label = '1-Specificity') plt.plot([0]+cuts.tolist()+[1], [0]+plot_data.y2.tolist()+[1], label = 'Sensitivity') # 添加参考线 plt.vlines(plot_data.cuts[max_ks_index], ymin = plot_data.y1[max_ks_index], ymax = plot_data.y2[max_ks_index], linestyles = '--') # 添加文本信息 plt.text(x = plot_data.cuts[max_ks_index]+0.01, y = plot_data.y1[max_ks_index]+plot_data.ks[max_ks_index]/2, s = 'KS= %.2f' %plot_data.ks[max_ks_index]) # 显示图例 plt.legend() # 显示图形 plt.show()

构建模型

案例1-绘制ks曲线

# 导入虚拟数据 virtual_data = pd.read_excel(r'virtual_data.xlsx') # 应用自定义函数绘制k-s曲线 plot_ks(y_test = virtual_data.Class, y_score = virtual_data.Score,positive_flag = 'P')

案例2-求解模型参数

# 读取数据 sports = pd.read_csv(r'Run or Walk.csv') # 提取出所有自变量名称 predictors = sports.columns[4:] # 构建自变量矩阵 X = sports.ix[:,predictors] # 提取y变量值 y = sports.activity # 将数据集拆分为训练集和测试集 X_train, X_test, y_train, y_test = model_selection.train_test_split(X, y, test_size = 0.25, random_state = 1234) # 利用训练集建模 sklearn_logistic = linear_model.LogisticRegression() sklearn_logistic.fit(X_train, y_train) # 返回模型的各个参数 print(sklearn_logistic.intercept_, sklearn_logistic.coef_)

Logistic回归模型参数

LogisticRegression(tol=0.0001, fit_intercept=True,class_weight=None, max_iter=100) # 参数 tol:⽤于指定模型跌倒收敛的阈值 fit_intercept:bool类型参数,是否拟合模型的截距项,默认为True class_weight:⽤于指定因变量类别的权重,如果为字典,则通过字典的形式{class_label:weight}传递每个类别的权重;如果为字符串'balanced',则每个分类的权重与实际样本中的⽐例成反⽐,当各分类存在严重不平衡时,设置为'balanced'会⽐较好;如果为None,则表示每个分类的权重相等 max_iter:指定模型求解过程中的最⼤迭代次数, 默认为100

模型预测结果统计

# 模型预测 sklearn_predict = sklearn_logistic.predict(X_test) # 预测结果统计 pd.Series(sklearn_predict).value_counts()

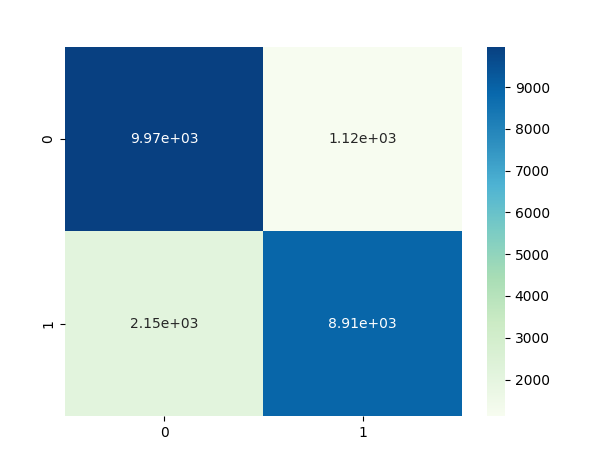

混淆矩阵

# 导入第三方模块 from sklearn import metrics # 混淆矩阵 cm = metrics.confusion_matrix(y_test, sklearn_predict, labels = [0,1])

模型准确率以及正反例覆盖率

Accuracy = metrics.scorer.accuracy_score(y_test, sklearn_predict) Sensitivity = metrics.scorer.recall_score(y_test, sklearn_predict) Specificity = metrics.scorer.recall_score(y_test, sklearn_predict, pos_label=0) print('模型准确率为%.2f%%:' %(Accuracy*100)) print('正例覆盖率为%.2f%%' %(Sensitivity*100)) print('负例覆盖率为%.2f%%' %(Specificity*100))

混淆矩阵的可视化—热力图

# 混淆矩阵的可视化 # 导入第三方模块 import seaborn as sns import matplotlib.pyplot as plt %matplotlib # 绘制热力图 sns.heatmap(cm, annot = True, fmt = '.2e',cmap = 'GnBu') # 图形显示 plt.show()

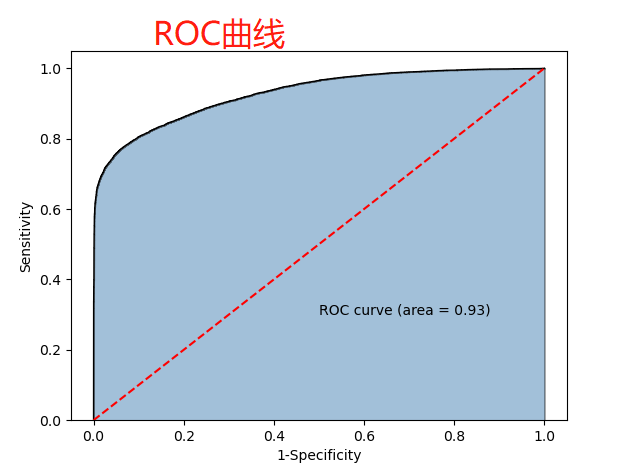

ROC曲线—面积图

计算折线下的⾯积,即阴影部分,这个⾯积称为AUC。

在做模型评估时,希望AUC的值越⼤越好,通常情况下,

当AUC在0.8以上时,说明模型基本准确。

# y得分为模型预测正例的概率 y_score = sklearn_logistic.predict_proba(X_test)[:,1] # 计算不同阈值下,fpr和tpr的组合值,其中fpr表示1-Specificity,tpr表示Sensitivity fpr,tpr,threshold = metrics.roc_curve(y_test, y_score) # 计算AUC的值 roc_auc = metrics.auc(fpr,tpr) # 绘制面积图 plt.stackplot(fpr, tpr, color='steelblue', alpha = 0.5, edgecolor = 'black') # 添加边际线 plt.plot(fpr, tpr, color='black', lw = 1) # 添加对角线 plt.plot([0,1],[0,1], color = 'red', linestyle = '--') # 添加文本信息 plt.text(0.5,0.3,'ROC curve (area = %0.2f)' % roc_auc) # 添加x轴与y轴标签 plt.xlabel('1-Specificity') plt.ylabel('Sensitivity') # 显示图形 plt.show()

# 调用自定义函数,绘制K-S曲线 plot_ks(y_test = y_test, y_score = y_score, positive_flag = 1)

Logistic回归模型的求解流程

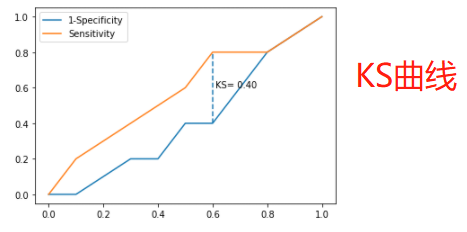

# -----------------------第一步 建模 ----------------------- # # 导入第三方模块 import statsmodels.api as sm # 将数据集拆分为训练集和测试集 X_train, X_test, y_train, y_test = model_selection.train_test_split(X, y, test_size = 0.25, random_state = 1234) # 为训练集和测试集的X矩阵添加常数列1 X_train2 = sm.add_constant(X_train) X_test2 = sm.add_constant(X_test) # 拟合Logistic模型 sm_logistic = sm.Logit(y_train, X_train2).fit() # 返回模型的参数 sm_logistic.params # -----------------------第二步 预测构建混淆矩阵 ----------------------- # # 模型在测试集上的预测 sm_y_probability = sm_logistic.predict(X_test2) # 根据概率值,将观测进行分类,以0.5作为阈值 sm_pred_y = np.where(sm_y_probability >= 0.5, 1, 0) # 混淆矩阵 cm = metrics.confusion_matrix(y_test, sm_pred_y, labels = [0,1]) cm # -----------------------第三步 绘制ROC曲线 ----------------------- # # 计算真正率和假正率 fpr,tpr,threshold = metrics.roc_curve(y_test, sm_y_probability) # 计算auc的值 roc_auc = metrics.auc(fpr,tpr) # 绘制面积图 plt.stackplot(fpr, tpr, color='steelblue', alpha = 0.5, edgecolor = 'black') # 添加边际线 plt.plot(fpr, tpr, color='black', lw = 1) # 添加对角线 plt.plot([0,1],[0,1], color = 'red', linestyle = '--') # 添加文本信息 plt.text(0.5,0.3,'ROC curve (area = %0.2f)' % roc_auc) # 添加x轴与y轴标签 plt.xlabel('1-Specificity') plt.ylabel('Sensitivity') # 显示图形 plt.show() # -----------------------第四步 绘制K-S曲线 ----------------------- # # 调用自定义函数,绘制K-S曲线 sm_y_probability.index = np.arange(len(sm_y_probability)) plot_ks(y_test = y_test, y_score = sm_y_probability, positive_flag = 1) """ 模型评估方法 """ 1.ROC曲线:通过计算AUC阴影部分的面积来判断模型是否合理(通常大于0.8表示OK) 2.KS曲线:通过计算两条折现之间最大距离来衡量模型是否合理(通常大于0.4表示OK)

-

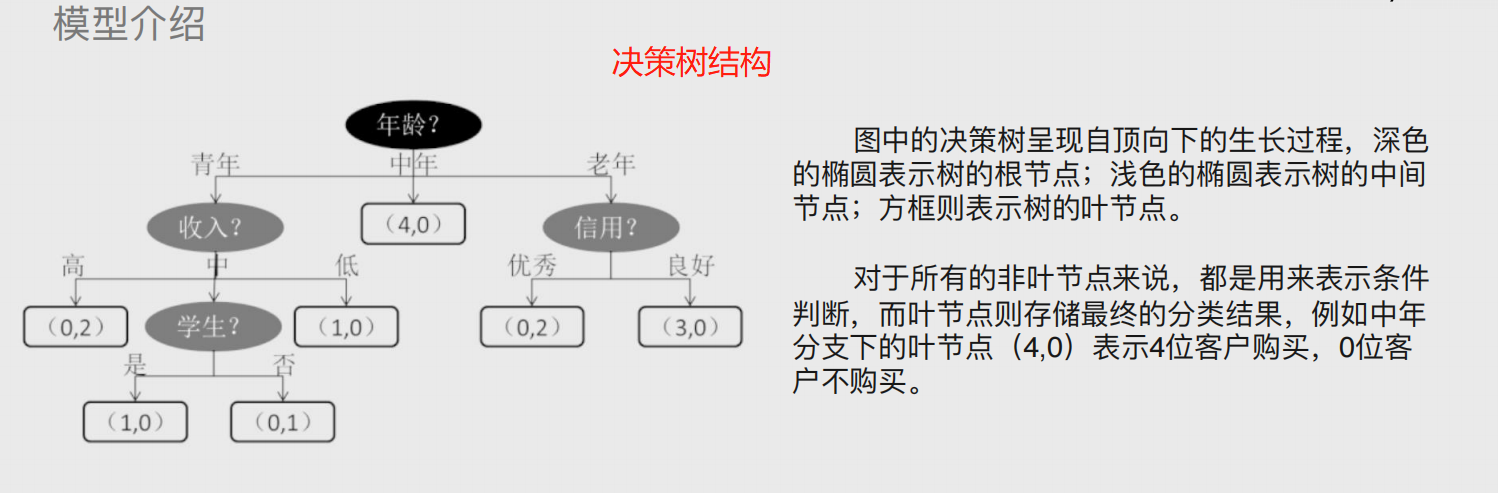

决策树与随机森林

决策树与随机森林:顾名思义,通常用于解决分类(决策)问题,即买不买,带不带,走不走等;也可以用来解决预测问题,即具体数值。

树的概念

这里的树其实是计算机底层的一种数据结构,与现实不同,可理解为自上而下生长 # 决策树 算法模型的概念,由三部分组成 根节点:树的起点 枝节点:即中间节点,和根节点一样也是条件判断 叶子节点:分支的终点

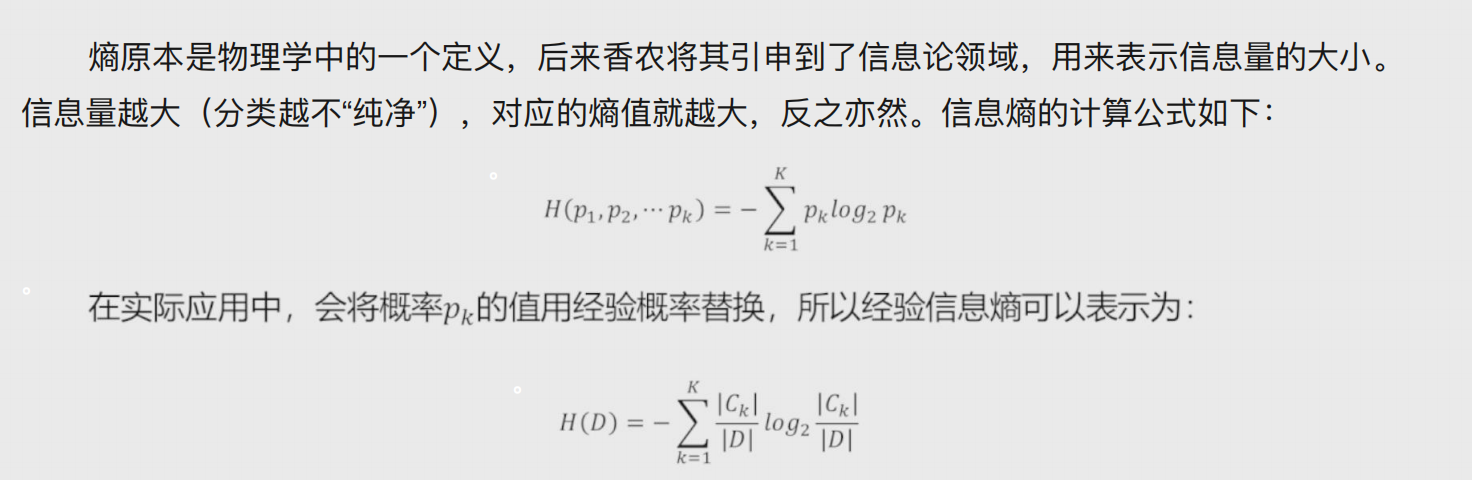

信息熵

熵原本是物理学概念,表示混乱程度;后被引用至信息领域,表示信息量的大小。

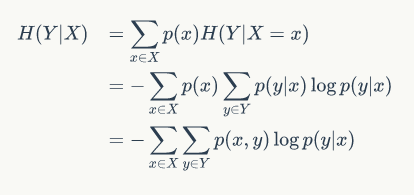

条件熵

条件熵为信息熵的引申,指添加条件后对信息熵进行分类。

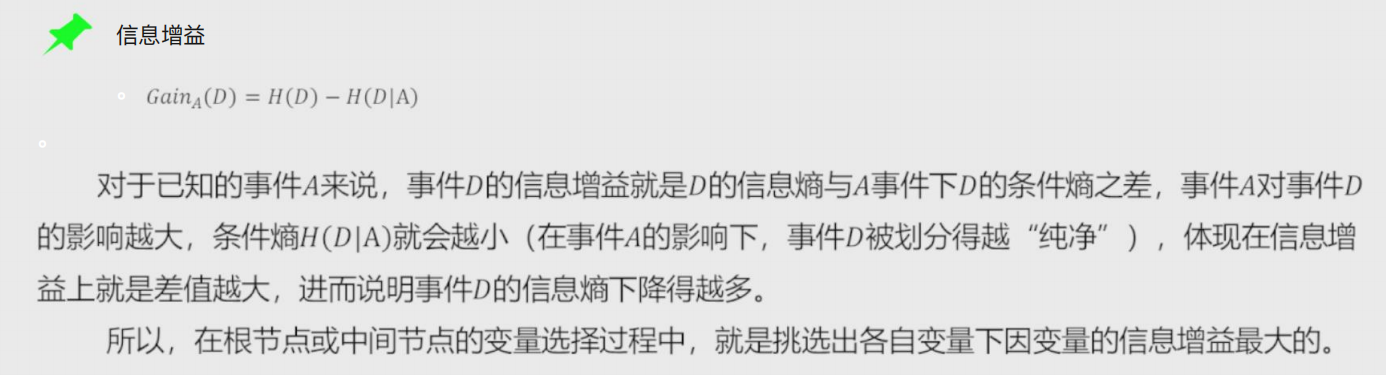

信息增益

用某个条件对原变量分类后,降低了原变量的不确定性。结论,不确定性减少程度就是信息的增益。

构建决策树时,根节点与枝节点存储的条件按照信息增益从大到小排列,即影响越大的条件在构建决策树的时候越靠近根节点!!!

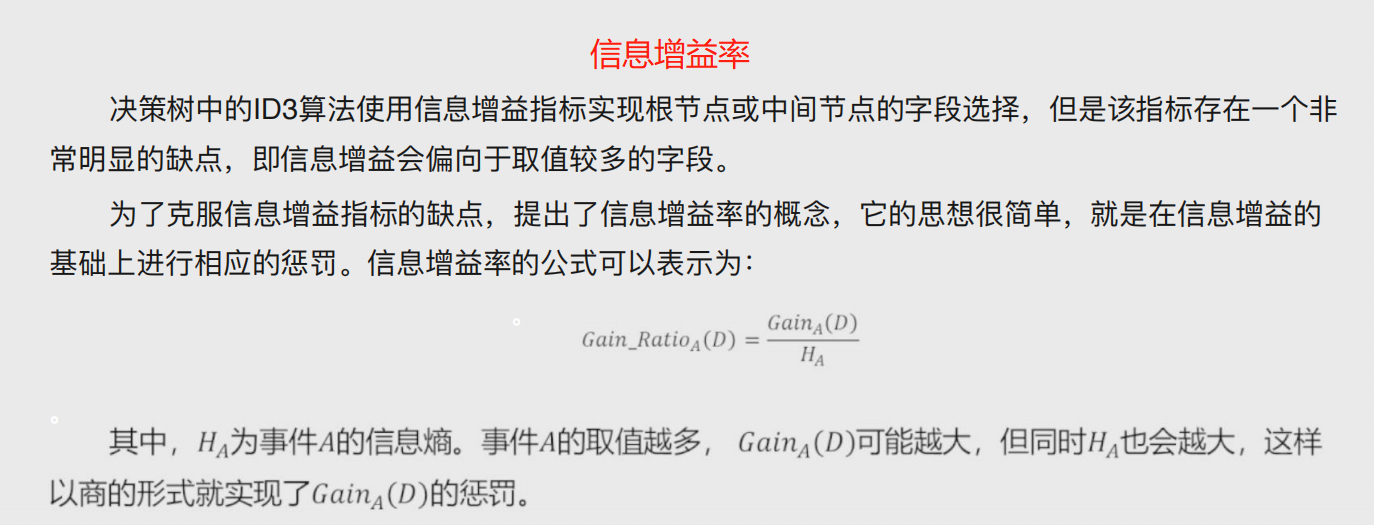

信息增益率

信息增益会偏向于取值较多的字段,为了避免,提出了信息增益率的概念,就是在计算信息增益时添加的惩罚项。

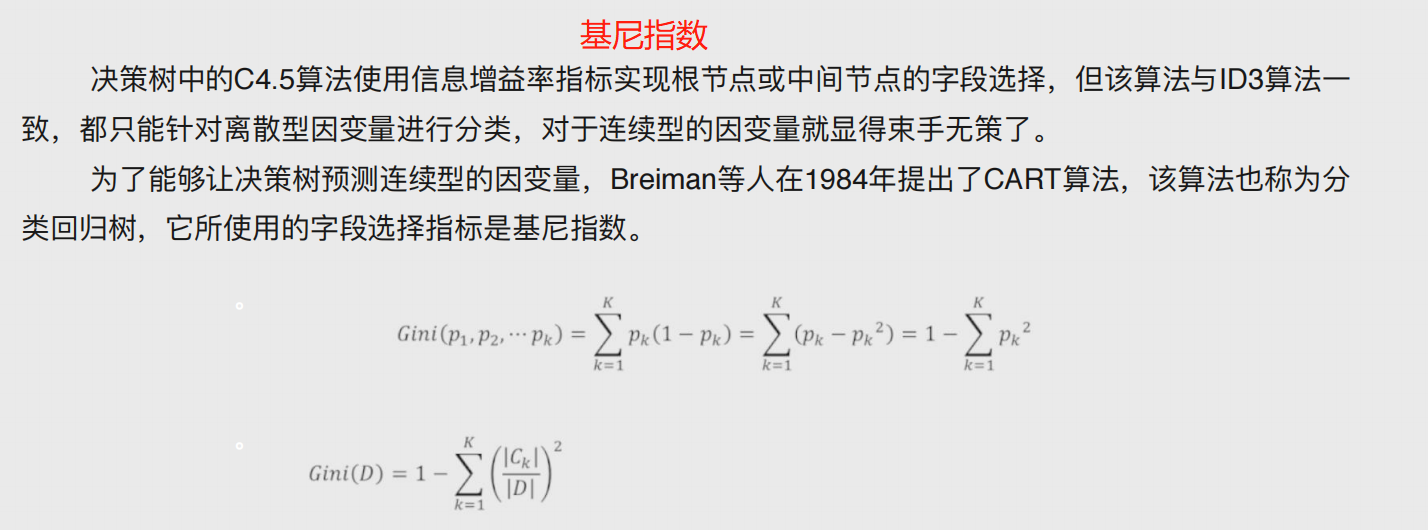

基尼指数

将模型数学化,从而能够解决连续性变量问题即预测性问题

基尼指数越小,说明数据集纯度越高,不确定性就越小,就越容易区分。

基尼指数增益

自变量对因变量的影响程度。

决策树参数说明

DecisionTreeClassifier(criterion='gini', splitter='best', max_depth=None,min_samples_split=2, min_samples_leaf=1,max_leaf_nodes=None, class_weight=None) # 参数 criterion:⽤于指定选择节点字段的评价指标,对于分类决策树,默认为'gini',表示采⽤基尼指数选 择节点的最佳分割字段;对于回归决策树,默认为'mse',表示使⽤均⽅误差选择节点的最佳分割字段 splitter:⽤于指定节点中的分割点选择⽅法,默认为'best',表示从所有的分割点中选择最佳分割点; 如果指定为'random',则表示随机选择分割点 max_depth:⽤于指定决策树的最⼤深度,默认为None,表示树的⽣⻓过程中对深度不做任何限制 min_samples_split:⽤于指定根节点或中间节点能够继续分割的最⼩样本量, 默认为2 min_samples_leaf:⽤于指定叶节点的最⼩样本量,默认为1 max_leaf_nodes:⽤于指定最⼤的叶节点个数,默认为None,表示对叶节点个数不做任何限制 class_weight:⽤于指定因变量中类别之间的权重,默认为None,表示每个类别的权重都相等;如果 为balanced,则表示类别权重与原始样本中类别的⽐例成反⽐;还可以通过字典传递类别之间的权重 差异,其形式为{class_label:weight}

决策树案例

# 导入第三方模块 import pandas as pd import numpy as np import matplotlib.pyplot as plt from sklearn import model_selection from sklearn import linear_model # 读⼊数据 Titanic = pd.read_csv(r'Titanic.csv') Titanic # 删除⽆意义的变量,并检查剩余变量是否含有缺失值 Titanic.drop(['PassengerId','Name','Ticket','Cabin'], axis = 1, inplace = True) Titanic.isnull().sum(axis = 0) # 对Sex分组,⽤各组乘客的平均年龄填充各组中的缺失年龄 fillna_Titanic = [] for i in Titanic.Sex.unique(): update = Titanic.loc[Titanic.Sex == i,].fillna(value = {'Age': Titanic.Age[Titanic.Sex == i].mean()}, inplace = False) fillna_Titanic.append(update) Titanic = pd.concat(fillna_Titanic) # 使⽤Embarked变量的众数填充缺失值 Titanic.fillna(value = {'Embarked':Titanic.Embarked.mode()[0]}, inplace=True) # 将数值型的Pclass转换为类别型,否则⽆法对其哑变量处理 Titanic.Pclass = Titanic.Pclass.astype('category') # 哑变量处理 dummy = pd.get_dummies(Titanic[['Sex','Embarked','Pclass']]) # ⽔平合并Titanic数据集和哑变量的数据集 Titanic = pd.concat([Titanic,dummy], axis = 1) # 删除原始的Sex、Embarked和Pclass变量 Titanic.drop(['Sex','Embarked','Pclass'], inplace=True, axis = 1) # 取出所有⾃变量名称 predictors = Titanic.columns[1:] # 将数据集拆分为训练集和测试集,且测试集的⽐例为25% X_train, X_test, y_train, y_test = model_selection.train_test_split(Titanic[predictors], Titanic.Survived, test_size = 0.25, random_state = 1234) from sklearn.model_selection import GridSearchCV from sklearn import tree,metrics # 预设各参数的不同选项值 max_depth = [2,3,4,5,6] min_samples_split = [2,4,6,8] min_samples_leaf = [2,4,8,10,12] # 将各参数值以字典形式组织起来 parameters = {'max_depth':max_depth, 'min_samples_split':min_samples_split, 'min_samples_leaf':min_samples_leaf} # ⽹格搜索法,测试不同的参数值 grid_dtcateg = GridSearchCV(estimator = tree.DecisionTreeClassifier(), param_grid = parameters, cv=10) # 模型拟合 grid_dtcateg.fit(X_train, y_train) # 返回最佳组合的参数值 grid_dtcateg.param_grid # 构建分类决策树 CART_Class = tree.DecisionTreeClassifier(max_depth=3,min_samples_leaf=4,min_samples_split=2) # 模型拟合 decision_tree = CART_Class.fit(X_train,y_train) # 模型在测试集上的预测 pred = CART_Class.predict(X_test) # 模型的准确率 print('模型在测试集的预测准确率:\n',metrics.accuracy_score(y_test,pred)) print('模型在训练集的预测准确率:\n',metrics.accuracy_score(y_train,CART_Class.predict(X_train)))

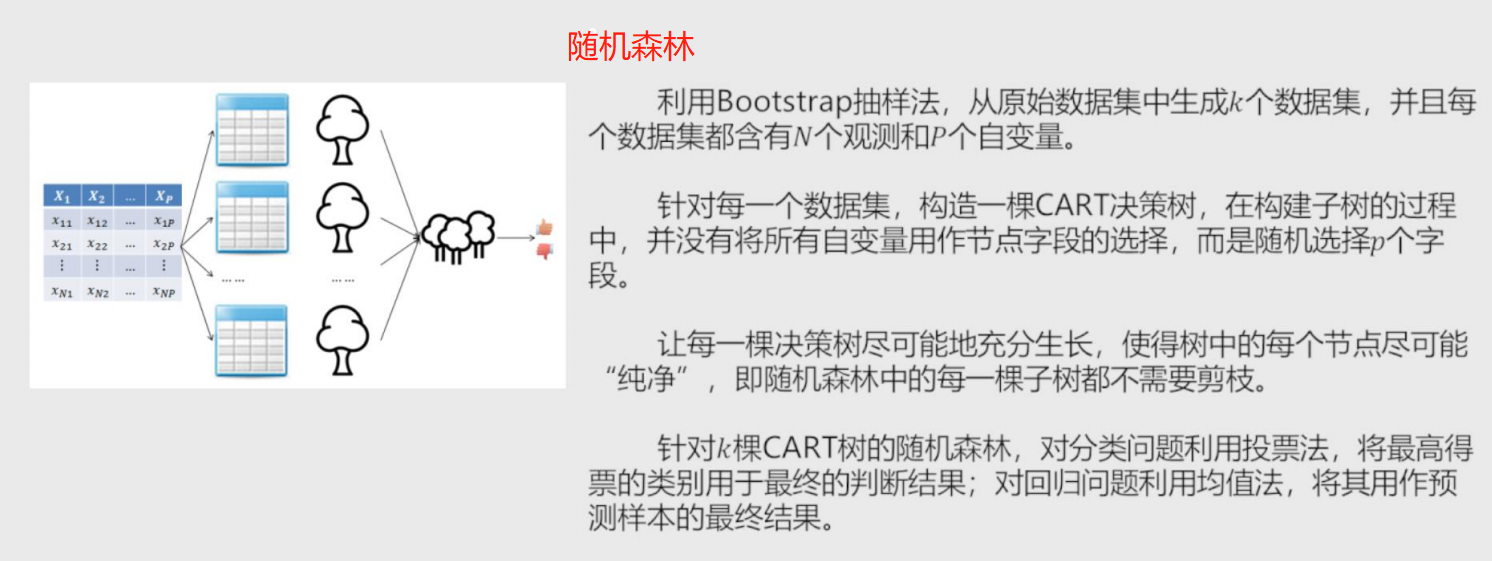

随机森林

由每颗决策树随机选择条件节点构成

对于分类问题使用投票法即选择树

对于回归问题使用均值法即求解回归模型参数

-

K近邻模型

该模型既可以解决分类问题 也可以解决预测问题。

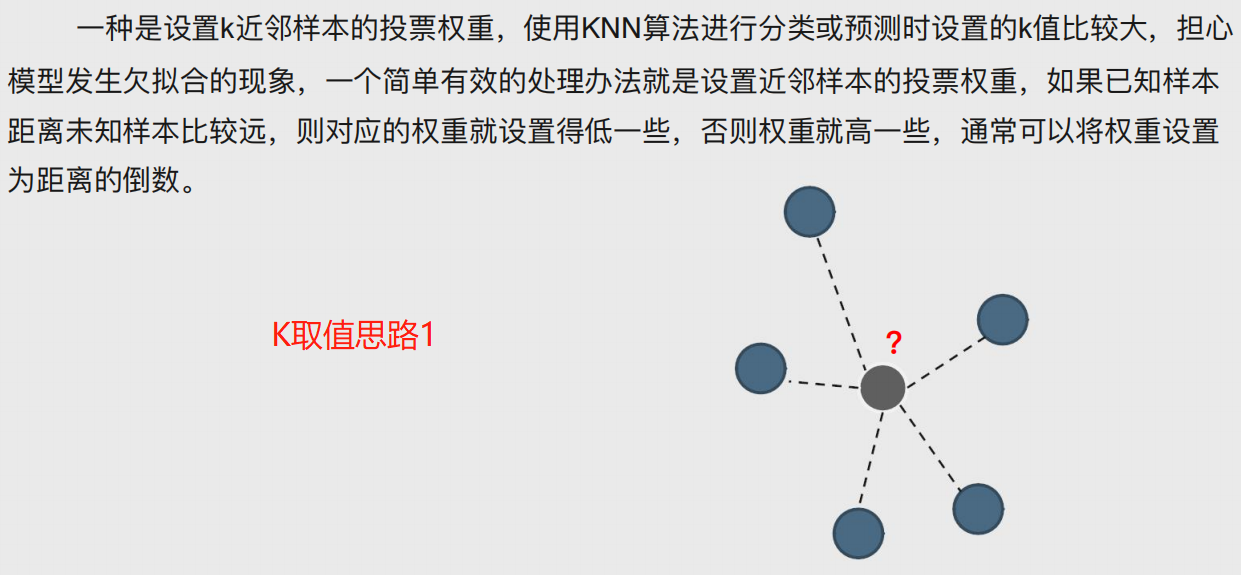

本质就是根据位置样本周边K个邻居样本做出预测。

K如何取值合适???不能过拟合也不能欠拟合。

过拟合:精确度过高

欠拟合:精确度过低

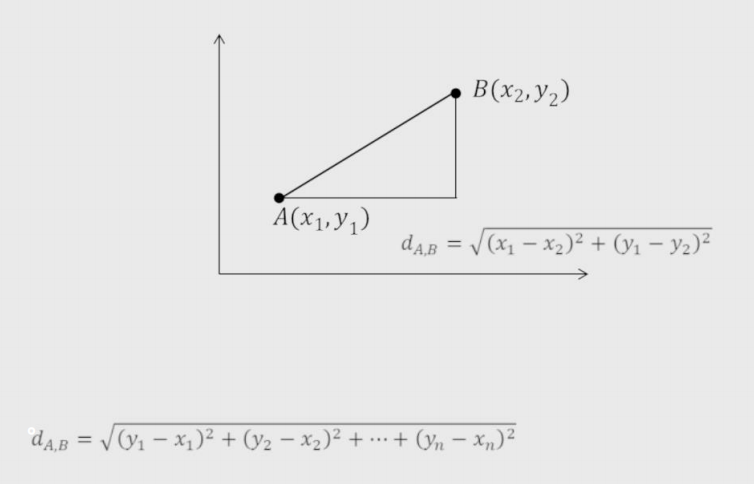

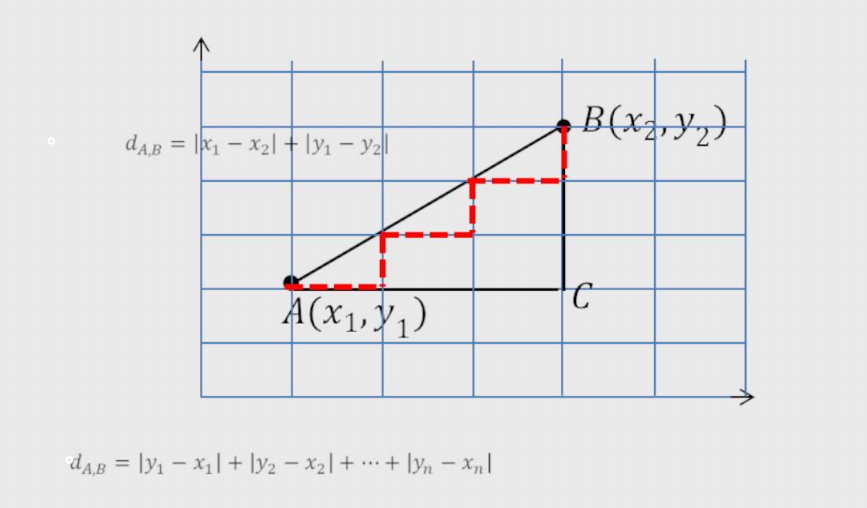

距离

1、欧氏距离:两点间直线距离。

2、曼哈顿距离:两点间绕过障碍物的距离。

3、余弦相似度:测量两个向量的夹角的余弦值来度量它们之间的相似性,可以用于论文查重。

KNN模型参数说明

neighbors.KNeighborsClassifier(n_neighbors=5, weights='uniform',p=2, metric='minkowski',) # 参数 n_neighbors:⽤于指定近邻样本个数K,默认为5 weights:⽤于指定近邻样本的投票权重,默认为'uniform',表示所有近邻样本的投票权重⼀样;如果 为'distance',则表示投票权重与距离成反⽐,即近邻样本与未知类别的样本点距离越远,权重越⼩, 反之,权重越⼤ metric:⽤于指定距离的度量指标,默认为闵可夫斯基距离 p:当参数metric为闵可夫斯基距离时,p=1,表示计算点之间的曼哈顿距离;p=2,表示计算点之间的欧⽒距离,默认值为2

KNN模型代码实现

案例1

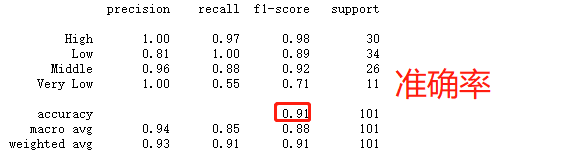

# 导入第三方包 import pandas as pd # 导入数据 Knowledge = pd.read_excel(r'Knowledge.xlsx') # 返回前5行数据 Knowledge.head() # 构造训练集和测试集 # 导入第三方模块 from sklearn import model_selection # 将数据集拆分为训练集和测试集 predictors = Knowledge.columns[:-1] predictors X_train, X_test, y_train, y_test = model_selection.train_test_split(Knowledge[predictors], Knowledge.UNS,test_size = 0.25, random_state = 1234) # 导入第三方模块 import numpy as np from sklearn import neighbors import matplotlib.pyplot as plt # 设置待测试的不同k值 K = np.arange(1,np.ceil(np.log2(Knowledge.shape[0]))).astype(int) # 构建空的列表,用于存储平均准确率 accuracy = [] for k in K: # 使用10重交叉验证的方法,比对每一个k值下KNN模型的预测准确率 cv_result = model_selection.cross_val_score(neighbors.KNeighborsClassifier(n_neighbors = k, weights = 'distance'), X_train, y_train, cv = 10, scoring='accuracy') accuracy.append(cv_result.mean()) # 从k个平均准确率中挑选出最大值所对应的下标 arg_max = np.array(accuracy).argmax() # 中文和负号的正常显示 plt.rcParams['font.sans-serif'] = ['Microsoft YaHei'] plt.rcParams['axes.unicode_minus'] = False # 绘制不同K值与平均预测准确率之间的折线图 plt.plot(K, accuracy) # 添加点图 plt.scatter(K, accuracy) # 添加文字说明 plt.text(K[arg_max], accuracy[arg_max], '最佳k值为%s' %int(K[arg_max])) # 显示图形 plt.show() # 导入第三方模块 from sklearn import metrics # 重新构建模型,并将最佳的近邻个数设置为6 knn_class = neighbors.KNeighborsClassifier(n_neighbors = 6, weights = 'distance') # 模型拟合 knn_class.fit(X_train, y_train) # 模型在测试数据集上的预测 predict = knn_class.predict(X_test) # 构建混淆矩阵 cm = pd.crosstab(predict,y_test) cm # 导入第三方模块 import seaborn as sns # 将混淆矩阵构造成数据框,并加上字段名和行名称,用于行或列的含义说明 cm = pd.DataFrame(cm) # 绘制热力图 sns.heatmap(cm, annot = True,cmap = 'GnBu') # 添加x轴和y轴的标签 plt.xlabel(' Real Lable') plt.ylabel(' Predict Lable') # 图形显示 plt.show() # 模型整体的预测准确率 metrics.scorer.accuracy_score(y_test, predict) # 分类模型的评估报告 print(metrics.classification_report(y_test, predict))

案例2

# 读入数据 ccpp = pd.read_excel(r'CCPP.xlsx') ccpp.head() # 返回数据集的行数与列数 ccpp.shape ################################################### # 导入第三方包 from sklearn.preprocessing import minmax_scale # 对所有自变量数据作标准化处理(统一量纲) predictors = ccpp.columns[:-1] X = minmax_scale(ccpp[predictors]) ################################################### # 将数据集拆分为训练集和测试集 X_train, X_test, y_train, y_test = model_selection.train_test_split(X, ccpp.PE, test_size = 0.25, random_state = 1234) # 设置待测试的不同k值 K = np.arange(1,np.ceil(np.log2(ccpp.shape[0]))).astype(int) # 构建空的列表,用于存储平均MSE mse = [] for k in K: # 使用10重交叉验证的方法,比对每一个k值下KNN模型的计算MSE cv_result = model_selection.cross_val_score(neighbors.KNeighborsRegressor(n_neighbors = k, weights = 'distance'), X_train, y_train, cv = 10, scoring='neg_mean_squared_error') mse.append((-1*cv_result).mean()) # 从k个平均MSE中挑选出最小值所对应的下标 arg_min = np.array(mse).argmin() # 绘制不同K值与平均MSE之间的折线图 plt.plot(K, mse) # 添加点图 plt.scatter(K, mse) # 添加文字说明 plt.text(K[arg_min], mse[arg_min] + 0.5, '最佳k值为%s' %int(K[arg_min])) # 显示图形 plt.show() # 重新构建模型,并将最佳的近邻个数设置为7 knn_reg = neighbors.KNeighborsRegressor(n_neighbors = 7, weights = 'distance') # 模型拟合 knn_reg.fit(X_train, y_train) # 模型在测试集上的预测 predict = knn_reg.predict(X_test) # 计算MSE值 metrics.mean_squared_error(y_test, predict) # 导入第三方模块 from sklearn import tree # 预设各参数的不同选项值 max_depth = [19,21,23,25,27] min_samples_split = [2,4,6,8] min_samples_leaf = [2,4,8,10,12] parameters = {'max_depth':max_depth, 'min_samples_split':min_samples_split, 'min_samples_leaf':min_samples_leaf} # 网格搜索法,测试不同的参数值 grid_dtreg = model_selection.GridSearchCV(estimator = tree.DecisionTreeRegressor(), param_grid = parameters, cv=10) # 模型拟合 grid_dtreg.fit(X_train, y_train) # 返回最佳组合的参数值 grid_dtreg.best_params_ # 构建用于回归的决策树 CART_Reg = tree.DecisionTreeRegressor(max_depth = 25, min_samples_leaf = 10, min_samples_split = 4) # 回归树拟合 CART_Reg.fit(X_train, y_train) # 模型在测试集上的预测 pred = CART_Reg.predict(X_test) # 计算衡量模型好坏的MSE值 metrics.mean_squared_error(y_test, pred)

浙公网安备 33010602011771号

浙公网安备 33010602011771号