Financial Reporting and Analysis 7

R21:Inventories

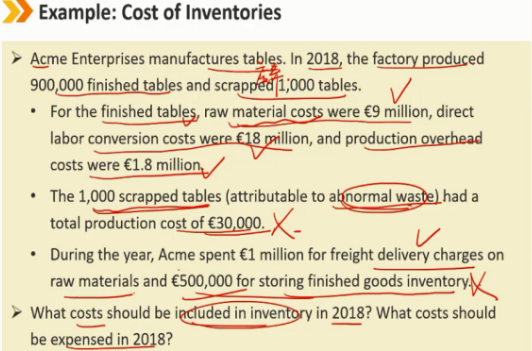

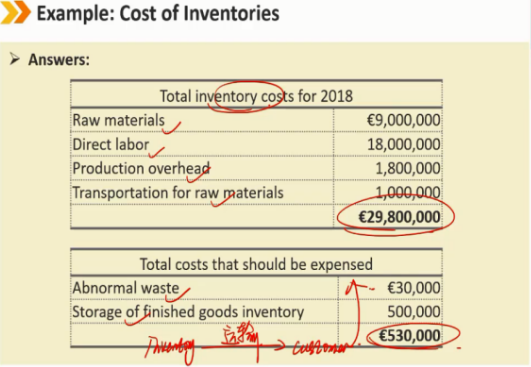

1、Cost of Inventories:存货成本

<1> The costs include in inventory are similar under IFRS and U.S. GAAP:

根据国际会计准则和美国会计准则,存货中包含的成本类似。资本化 -> COGS

Costs of purchase(less trade discounts and rebates):购置成本(减去贸易折扣和回扣)

- Include purchase price, import and tax-related duties, transport and insurance during transport, handling.

- 包括采购价格、进口税、运输和装卸期间的运费和保险。

Costs of conversion:转换成本(把购买进来的原材料加工成在产品、完成品的过程产生的成本费用)

- Such as direct labor and fixed and variable overhead costs

- 如直接人工和固定及可变间接费用

Other costs necessary to bring the inventory to its present location and condition.

使存货达到可销售的位置和状态所需的其他费用。

基本上是在存货在到达 ready for sale 之前产生的费用

<2> Both IFRS and US GAAP exclude the following costs from inventory:

国际会计准则和美国会计准则均不包括以下存货成本:费用化

Abnormal costs due to waste.

由于浪费而产生的异常成本。

例如:生产木材家具产生的一些边角料可以算作存货成本,但是如果因为管理不当,仓库漏水把木材都泡了导致的损失,只能算作异常浪费而产生的费用。

Storage costs of finished inventory. ( unless required as part of the production process)

成品库存的储存成本。(除非贮藏成本是生产过程中必不可少的组成部分,例如红酒贮藏)

例如:成品产生的库存费用,是因为没有尽快将成品销售出去,从而也算是管理不善导致的费用。

All administrative and selling costs.(SG&A)

所有管理和销售成本(给客户输出成品产生的运输费等)。

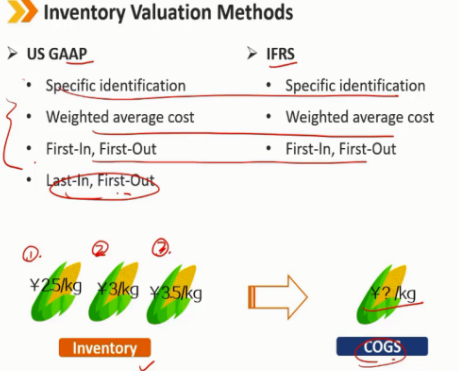

2、Inventory Valuation Methods:存货估值(计价)方法

2.1 Inventory Valuation Methods

美国会计准则下独有 LIFO

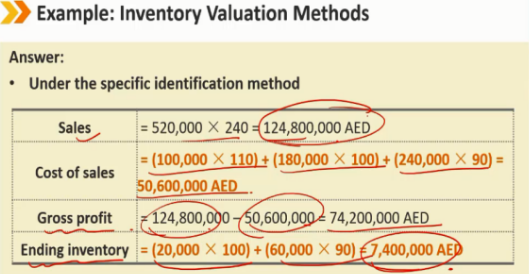

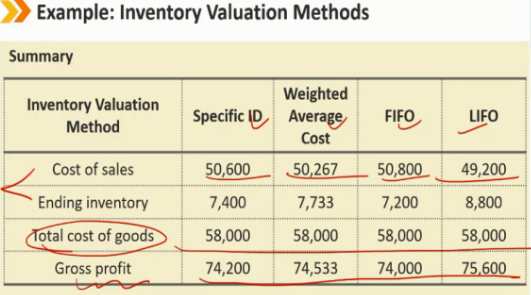

(1)Specific identification:个别识别法This method matches the physical flow of the specific items sold and remaining in inventory to their actual cost.

此方法将已售出和库存中剩余的特定项目的物理流与其实际成本相匹配。

The method is used for inventory items that are not ordinarily interchangeable and for expensive goods that are uniquely identifiable.

该方法用于通常不可互换的库存物品和唯一可识别的昂贵物品。

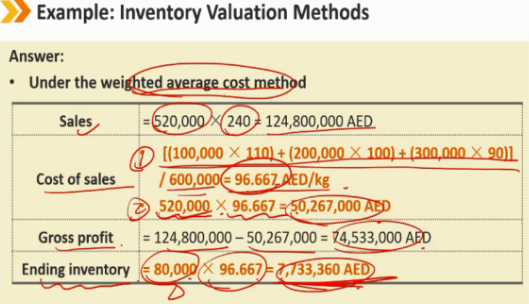

(2)Weighted average cost:加权平均成本法

This method assigns the average cost of the goods available for sale to the units that are sold as well as to the units in ending inventory.

此方法将可供销售商品的平均成本分配给已销售的单位以及期末存货中的单位。

Total cost of goods available for sale / Total units available for sale

可供出售商品的总成本 / 可供出售的总单位

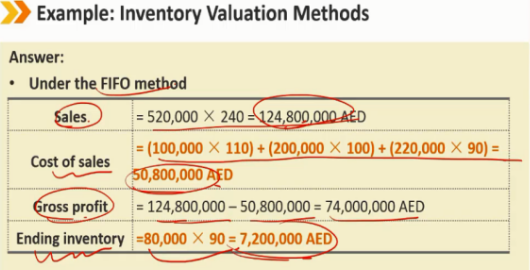

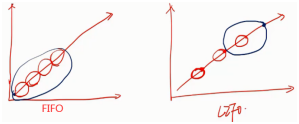

(3)First-In, First-Out(FIFO):先进先出法

FIFO assumes that the oldest goods purchased (or manufactured) are sold first and the newest goods purchased (or manufactured) remain in ending inventory.

先进先出假设购买或制造的最旧商品先售出,购买(或制造)的最新商品仍保留在期末存货中。

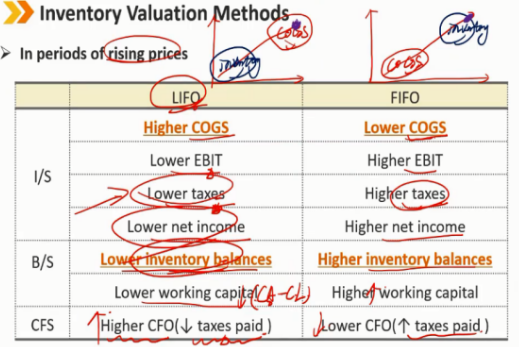

In periods of rising prices, the costs assigned to the units in ending inventory are higher than the costs assigned to the units sold.

在价格上涨期间,期末存货中分配给单位的成本高于分配给售出单位的成本。

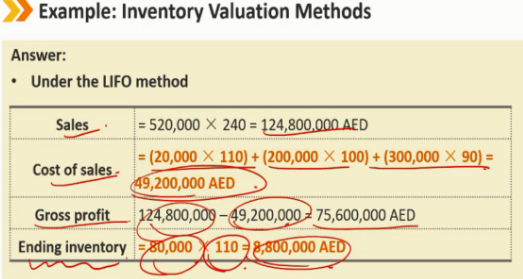

(4)Last-In, First-Out(LIFO):后进先出法

LIFO is permitted only under US GAAP.

后进先出法仅在美国会计准则下允许。

LIFO assumes that the newest goods purchased (or manufactured) are sold first and the oldest goods purchased (or manufactured) remain in ending inventory.

后进先出法假设购买(或制造)的最新商品先售出,购买(或制造)的最旧商品仍保留在期末存货中。

In periods of rising prices, the costs assigned to the units in ending inventory are lower than the costs assigned to the units sold.

在价格上涨期间,期末存货中分配给单位的成本低于分配给售出单位的成本。

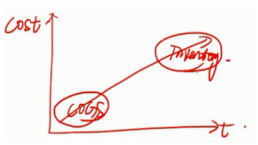

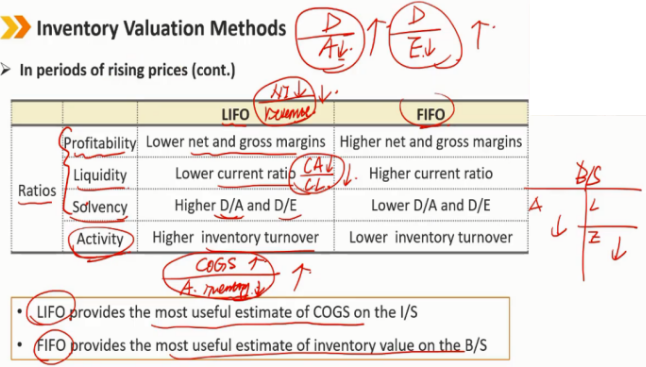

采用LIFO,虽然Net income,Asset变少,但是会使企业少交税

LIFO对比FIFO,盈利能力的指标都低,但是COGS的周转率高

LIFO下,因为COGS更贴近真实价格,所以对COGS的估计更有效,

反之,FIFO存货更贴近真实价格,所以对存货的估计更有效,

但是两者对于相应的另外的一项的价格都是低估

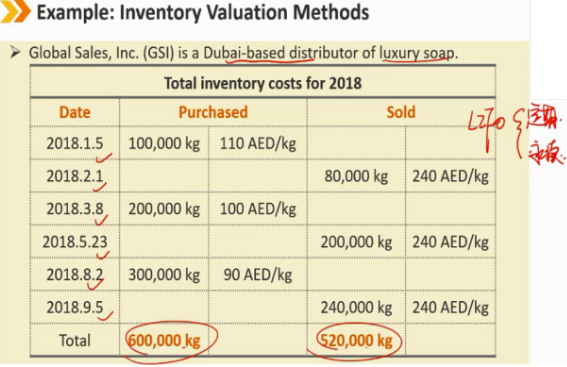

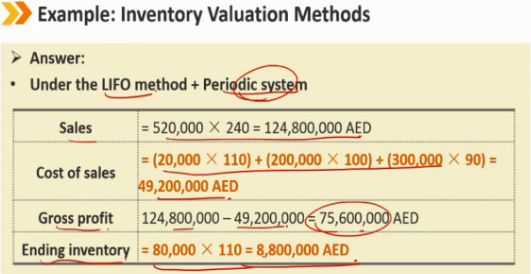

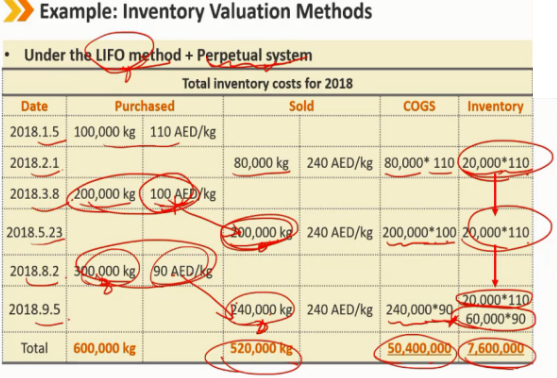

2.2 Periodic versus perpetual inventory systems:定期盘存法和永续盘存法对比

Under a periodic inventory system, inventory values and COGS are determined at the end of an accounting period.

在定期盘存制度下,存货价值和COGS在会计期末确定。

Under a perpetual inventory system, inventory values and COGS are continuously updated to reflect purchases and sales.

在永续盘存制度下,存货价值和COGS会不断更新,以反映购销情况。

Under either system, the allocation of goods available for sale to cost of sales and ending inventory is

在这两种制度中,可供销售的商品分配到销售成本和期末存货

- the same under specific identification and FIFO

- 在个别识别法和FIFO下相同

- usually different under weighted average cost method and LIFO

- 通常在加权平均成本法和LIFO下不同

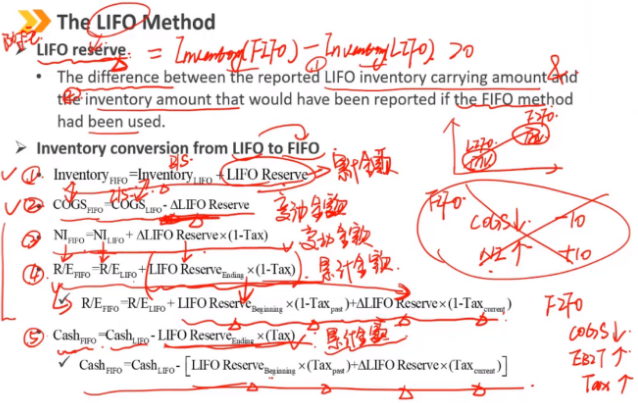

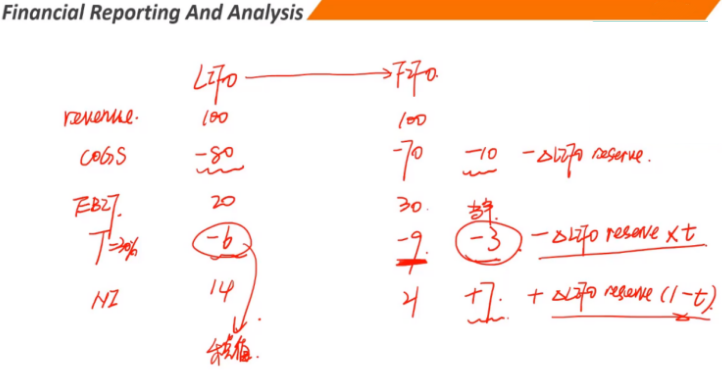

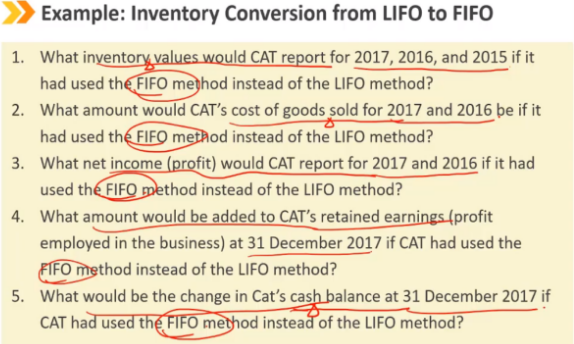

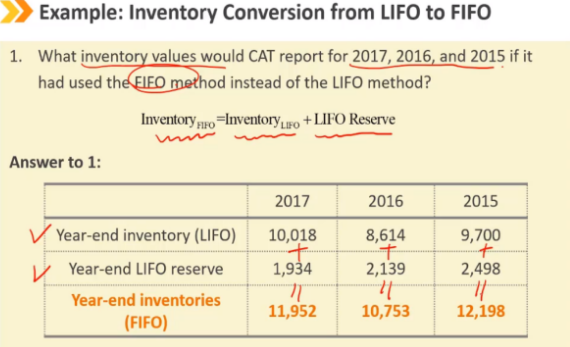

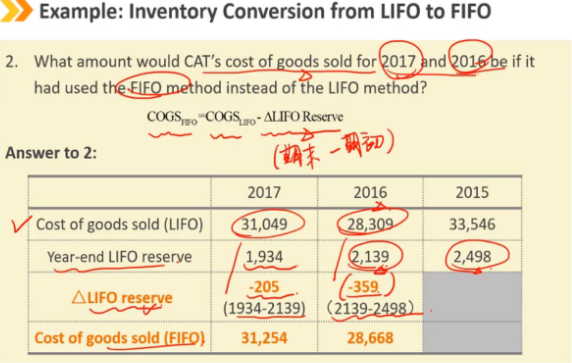

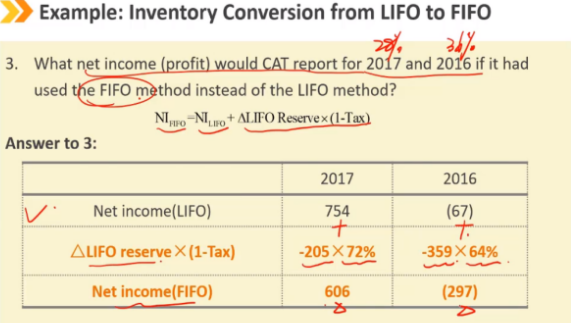

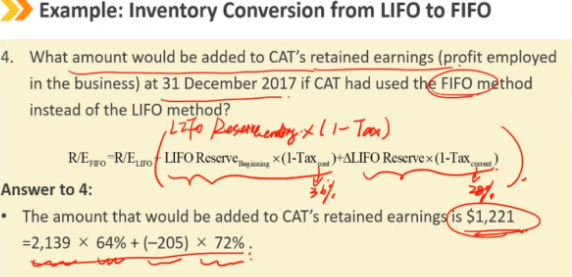

3、The LIFO Method:后进先出法

将使用LIFO方法的公司转化成FIFO方法下的估计,方便进行不同方法下公司盈利能力的对比

3.1 LIFO Reserve:后进先出准备金

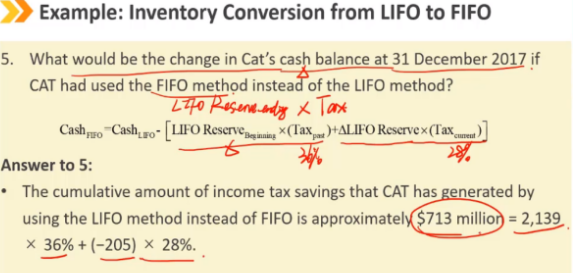

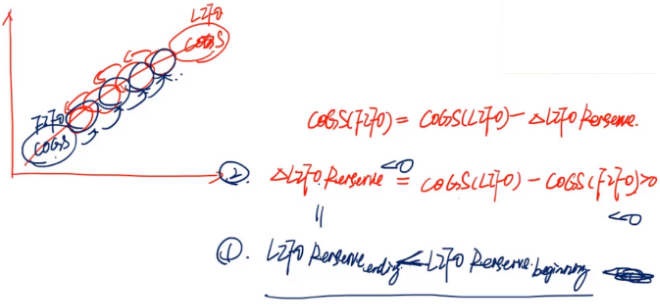

LIFO Reserve: FIFO存货 - LIFO存货 所报告的后进先出存货账面价值与采用先进先出法时本应报告的存货金额之间的差额 最基础的公式: Inventory(FIFO) = Inventory(LIFO) + LIFO Reserve COGS(FIFO) = COGS(LIFO) - △LIFO Reserve 现金是因为 LIFO 少交税,FIFO 多交税,所以 LIFO 现金多 △LIFO Reserve * t

3.2 LIFO liquidations:后进先出清算

A company using LIFO will experience a LIFO liquidation when the number of units sold exceeds the number of units purchased or manufactured.

当出售的单位数量超过购买或制造的单位数量时,使用后进先出法的公司将经历后进先出清算,即这段时间的货物的销售数量大于进货数量,已经开始不得不使用原来的存货用于销售。

If inventory unit costs have been rising from period to period and LIFO liquidation occurs, this will produce an increase in gross profits, but it is unsustainable.

如果存货单位成本在一个时期到另一个时期一直在上升,并且后进先出清算发生,这将产生毛利润的增加(因为不不断耗用之前进价低的老库存,COGS下降),但这是不可持续的。

出现LIFO liquidation现象的情况:(都不是好情况)

- In periods of economic recession or when customer demand is declining, a company may choose to reduce existing inventory levels.

- 在经济衰退时期或客户需求下降时,公司可能会选择降低现有库存水平。

- Management can potentially manipulate and inflate gross profits at critical times by intentionally reducing inventory quantities and liquidating older layers of LIFO inventory.

- 管理层可以在关键时刻通过故意减少库存数量和清算旧的后进先出库存来操纵和夸大毛利润。

A decline in the LIFO reserve may be indicative of LIFO liquidation.

后进先出准备金的减少可能表明出现了后进先出清算。

4、Inventory Method Changes:存货方法的改变

Companies on rare occasion change inventory valuation methods.

公司很少会改变存货估价方法。

- Under IFRS, the firm must demonstrate that the change will provide reliable and more relevant information. Under U.S. GAAP the firm must explain why the change in cost flow method is preferable.

- 根据国际会计准则,公司必须证明变更将提供可靠和更相关的信息。根据美国会计原则,公司必须解释为什么成本流动法的变更更可取。

In most cases, the change is made retrospectively.

在大多数情况下,变更是要对过去年份进行追溯性的。

- For example, if a company changes its inventory method in 2018 and the change would be reflected in the three years of financial statements presented. (2016, 2017, and 2018)

- 例如,如果一家公司在2018年改变了其存货方法,并且这种改变将反映在所列三年的财务报表中。(2016年、2017年和2018年)

An exception to the retrospective restatement is when a company reporting under US GAAP changes to the LIFO method.

追溯重述的一个例外情况是,根据美国会计原则报告的公司改变成为了后进先出法。

- In this case, the change is applied prospectively, the carrying amount of inventory under the old method becomes the initial LIFO layer in the year of LIFO adoption.

- 在这种情况下,变更是前瞻性应用的,不需要对历史时期进行追溯,旧方法下的存货账面价值成为采用后进先出法时的期初存货值。

5、Inventory Adjustments:存货调整

5.1 Under IFRS

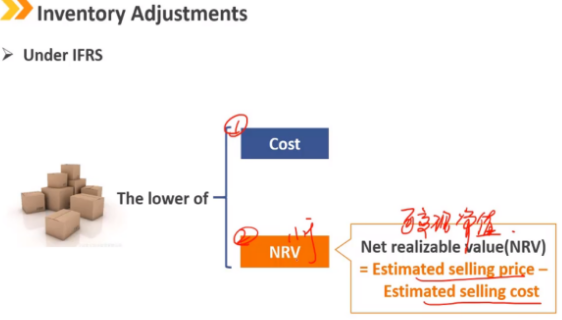

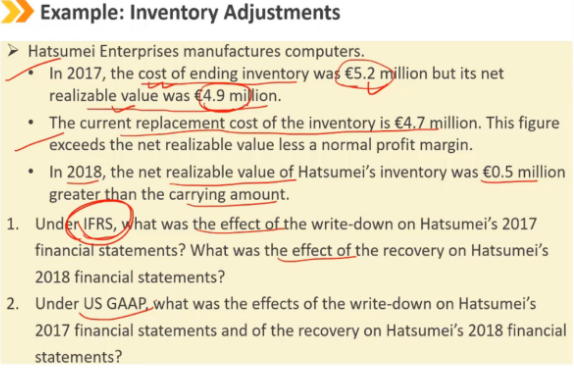

Cost:这批货的初始成本

NRV:可变现净值,指的是把这批存货卖掉留到手中的钱有多少

NRV = 估计的销售价格 - 估计的在销售过程中产生的成本

如果 Cost > NRV,则需要对存货进行减值,因为即使卖了这批存货也卖不出原先成本的那些钱

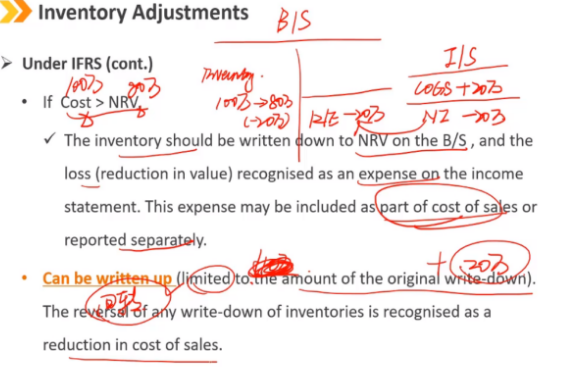

如果 Cost > NRV:

- 存货应在资产负债表上减值至NRV,损失(价值减少)在利润表上确认为费用。该费用可作为销售成本COGS的一部分或单独报告。

可回转(仅限于原始减值金额范围内)任何存货减值的回转确认为销售成本的减少,按原减值路径回转。

例如:Cost是100万,NRV为80万,则减值20万,之后如果存货价格又涨到110万,则只能回转到100万

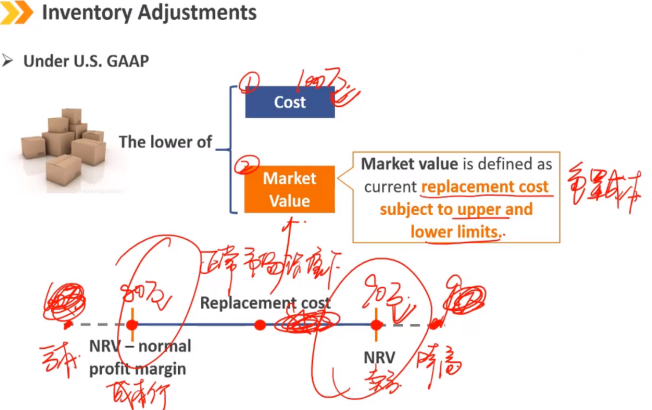

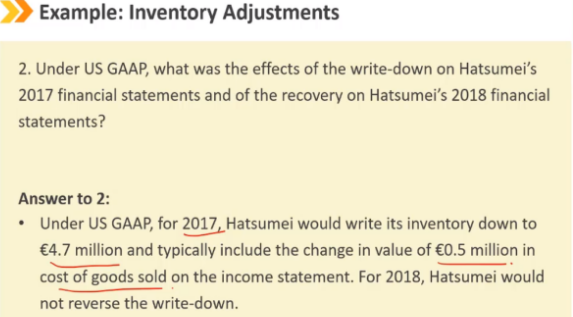

5.2 Under U.S. GAAP

Cost:这批货的初始成本

Market Value:重置成本,即按照当前的市场价格再去买这批存货需要的成本,要满足一个上下限要求,上限是 NRV,下限是 NRV - normal profit margin,NRV 减正常的利润部分,目的是为了保证重置价格是正常市场环境下的公允价格

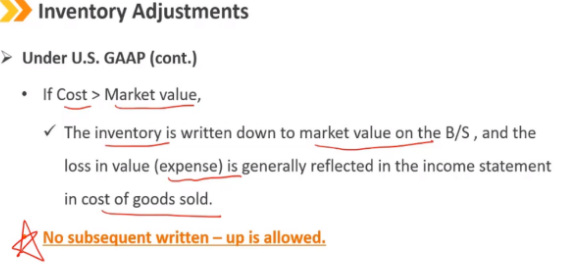

如果 Cost > 市场价值 Market Value

- 存货在资产负债表上减值到市场价值,价值损失(费用)通常反映在利润表中的销售成本COGS中。

不允许有后续的回转。

5.3 Note

注意:

- 国际会计准则允许农业产品和林业产品以及矿产和矿产品的生产商和经销商的存货以NRV可变现净值入账,即使高于历史成本。(美国会计原则的处理方法与此类似)

- 与使用后进先出法的公司相比,使用个别识别法、加权平均成本法或先进先出法的公司更可能发生存货减值。因为LIFO的存货估计已经比较低了。

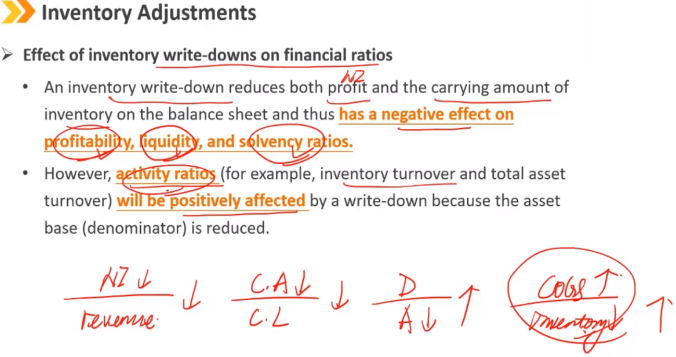

5.4 Effect of inventory write-downs on financial ratios:存货减值对财务比率的影响

存货减值会降低资产负债表上的利润和存货账面价值,从而对盈利能力、流动性和偿付能力比率产生负面影响。

然而,由于资产基数(分母)减少,减值将对营运比率(例如,存货周转率和总资产周转率)产生积极影响。

NI 下降;CA 下降;A下降导致偿债能力变弱;减值导致COGS增加,inventory下降,所以周转率变快

6、Evaluation of Inventory Management:存货管理的评估

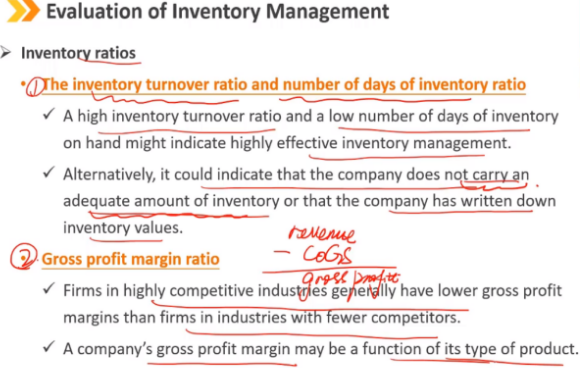

存货相关比率 1、存货周转率和存货周转率天数 - 较高的存货周转率和较低的存货周转天数可能意味着高效的存货管理 - 或者,它可能表明该公司没有携带足够的存货金额(比如企业的货在市场上供不应求,但是企业为了实现一个更好的存货周转率,没有提高存货的储备和生产,导致没有实现企业生产的最大化),或者该公司已对存货价值进行减值,这个时候也会体现一个较高的存货周转率,但是并不意味着企业的存货管理能力变强了 2、毛利率 - 竞争激烈行业的公司毛利率通常低于竞争对手较少行业的公司。 - 公司的毛利率可能是其产品类型的结果(例如生产衣服,较为平价的衣服的厂商的毛利率较低,高档衣服的厂商的毛利率较高)

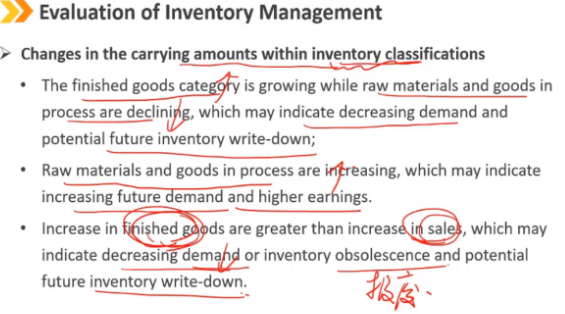

存货各类别中账面价值的变化(已完工产品、原材料、在产品的相应账面价值) - 已完工产品在增长,而原材料和在产品在下降,这可能表明市场需求在下降,未来可能出现存货减值 - 原材料和在产品增长,这可能表明未来市场需求增加,收入增加 - 已完工产品的增长大于销售额的增长,这可能表明市场需求在下降,或将出现存货报废,以及潜在的未来存货减值

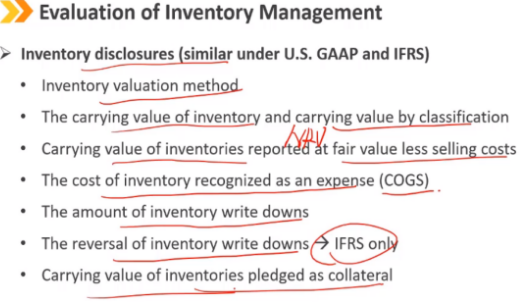

存货披露(美国会计准则和国际会计准则类似),在附注部分披露 存货估值方法 存货的账面金额和各个分类下的账面金额(原材料、在产品、已完工的产品等) 按公允价值减去销售成本报告的存货账面价值,即NRV 确认为费用的存货成本(即结转为COGS的存货价值) 存货减值的金额 存货减值回转的金额 —> 仅限国际会计准则 被企业拿去作为抵押品的存货账面价值

Summary:

浙公网安备 33010602011771号

浙公网安备 33010602011771号