Time Series_2_Cointegration and VAR

1. Cointegration

n×1 vector yt of time series is cointegrated if each series individually integrated in the order d (d = 1, nonstationary unit-root processes, i.e., random walks; d = 0, stationary process).

1.1 Simulation for Cointegration, based on Hamilton (1994)

![]()

![]()

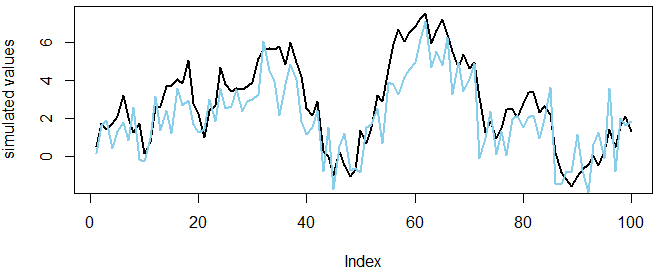

#generate the two time series of length 1000 set.seed(20200229) #fix the random seed N <- 100 #define length of simulation x <- cumsum(rnorm(N)) #simulate a normal random walk gamma <- 0.7 #set an initial parameter value y <- gamma * x + rnorm(N) #simulate the cointegrating series plot(x, col="black", type='l', lwd=2, ylab='simulated values') lines(y,col="skyblue", lwd=2)

Both series are individually random walks.

In real world we don't know gamma, so need estimation based on raw data, running linear regression of one series on the other, i.e., Engle-Granger method of testing cointegration.

1.2 Statistical Tests (Augmented Dickey Fuller test)

install.packages('urca')

library('urca')

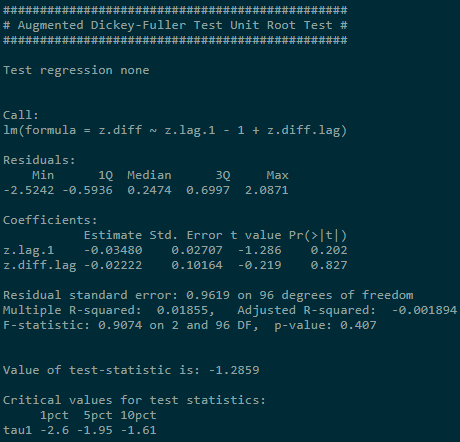

summary(ur.df(x,type="none"))

summary(ur.df(y,type="none"))

NULL: Unit root exists in the process

Reject NULL if test-statistic is smaller than critical value. Result shows test-statistic is larger than critical value at three usual sig.levels. We can't reject NULL.

Conclusion: Both series are individually unit root process.

1.3 Linear Combination

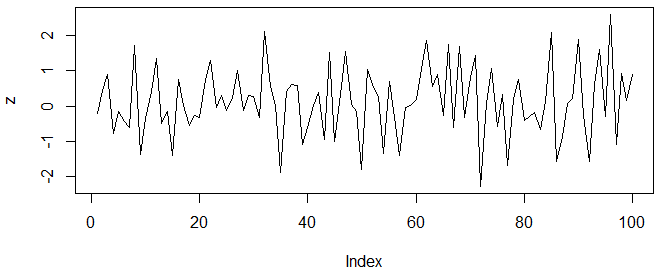

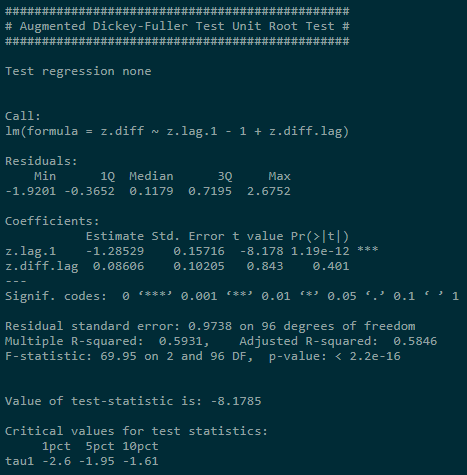

z <- y - gamma * x plot(z,type='l') summary(ur.df(z,type="none"))

zt seems to be a white noise process and rejection of unit root if confirmed by ADF tests:

1.4 Estimate the Cointegrating Relationship using Engle-Granger method

Step 1: Run linear regression yt on xt (simple OLS estimation);

Step 2: Test residuals for the presence of a unit root.

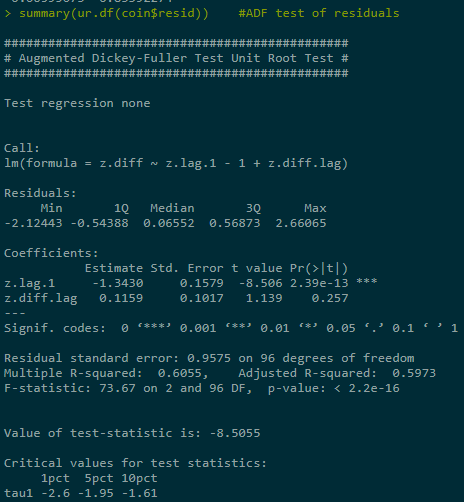

coin <- lm(y ~ x -1) #regression without constant coin$resid #obtain the residuals summary(ur.df(coin$resid)) #ADF test of residuals

Reject NULL.

Pair trading (statistical arbitrage) exploits such cointegrating relationship, aiming to set up strategy based on the spread between two time series. If two series are cointegrated, we expect their stationary linear combination to revert to 0. By selling relatively expensive and buying cheaper one, wait for the reversion to make profit.

Intuition: Linear combination of time series (which form cointegrating relationship) is determined by underlying (long-term) economic forces, e.g., same industry companies may grow similarly; spot and forward price of financial product are bound together by no-arbitrage principle; FX rates of interlinked countries tend to move together.

2. Vector Autoregressive Model

2.1 Theory Bgs

![]()

Ai are n×n coefficient matrices for all i = 1...p;

ut is a vector white noise process (assumes lack of auto correlation, while allow contemporaneous (同时发生的) correlation between components, i.e., ut has non-diagonal covariance matrix, meaning that contemporaneous dependencies aren't modeled) with positive definite covariance matrix. Thus we can use OLS to estimate equation by equation. (叫做 reduced form VAR models)

另一种叫做 structural VAR form model, SVAR models the contemporaneous effects among variables:

![]()

Where: ![]()

Disturbance terms are defined to be uncorrelated, thus are referred to as structural shocks.

2.2 Three-component VAR model (equity return, stock index, US Treasury bond interest rates)

2.2.1 Task: Forecast stock market index by using additional variables and identify impluse responses.

Assume: There exists a hidden long-term relationship between these three components.

2.2.2 Process:

rm(list = ls()) #clear the whole workspace

install.packages('xts');library(xts)

install.packages('vars');library('vars')

install.packages('quantmod');library('quantmod')

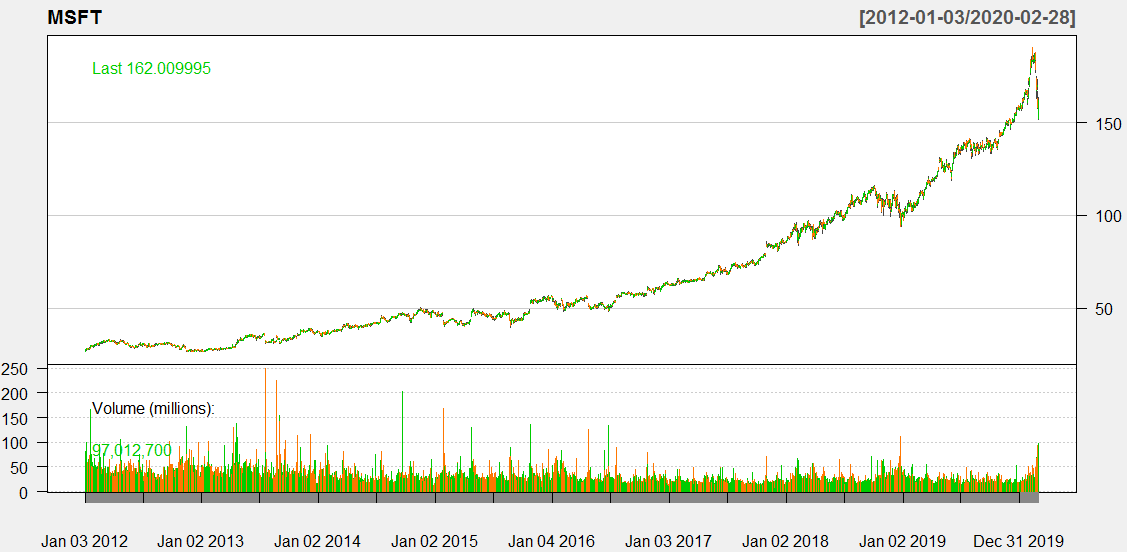

getSymbols('SNP', from='2012-01-02', to='2020-02-29')

getSymbols('MSFT', from='2012-01-02', to='2020-02-29')

getSymbols('DTB3', src='FRED') #3-month T-Bill interest rates

chartSeries(MSFT, theme=chartTheme('white'))

Cl(MSFT) #closing prices Op(MSFT) #open prices Hi(MSFT) #daily highest price Lo(MSFT) #daily lowest price ClCl(MSFT) #close-to-close daily return Ad(MSFT) #daily adjusted closing price

Subset to obtain period of interests ,while the downloaded prices are supposed to be nonstationary series and should be transformed into stationary series:

#indexing time series data DTB3.sub <- DTB3['2012-01-02/2020-02-29'] #Calculate returns from Adjusted log series SNP.ret <- diff(log(Ad(SNP))) MSFT.ret <- diff(log(Ad(MSFT))) #replace NA values DTB3.sub[is.na(DTB3.sub)] <- 0 DTB3.sub <- na.omit(DTB3.sub) # return with incomplete removed # merge the three databases to get the same length # innerjoin returns only rows in which one set have matching keys in the other dataDaily <- na.omit(merge(SNP.ret,MSFT.ret,DTB3.sub), join='inner')

VAR modeling usually deals with lower frequency data, so transform data to monthly (or quarterly) frequency.

#obtain monthly data, package xts SNP.M <- to.monthly(SNP.ret)$SNP.ret.Close MSFT.M <- to.monthly(MSFT.ret)$MSFT.ret.Close DTB3.M <- to.monthly(DTB3.sub)$DTB3.sub.Close

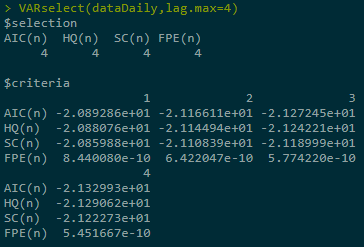

# allow a max of 4 lags # choose the model with best(lowest Akaike Information Criterion value) var1 <- VAR(dataDaily, lag.max=4, ic="AIC")

Or see multiple information criteria:

VARselect(dataDaily,lag.max=4)

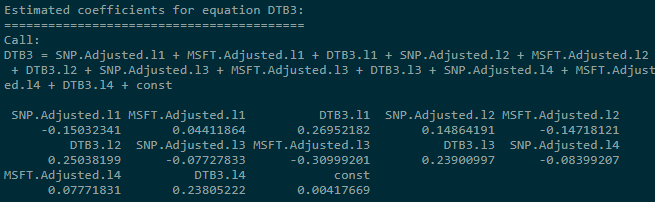

summary(var1)

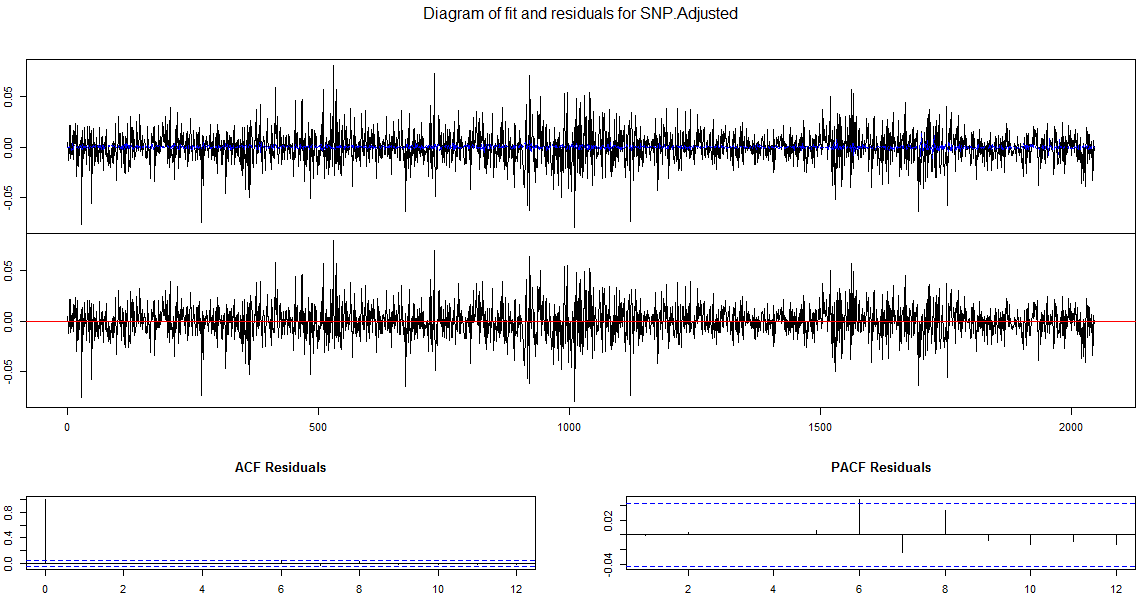

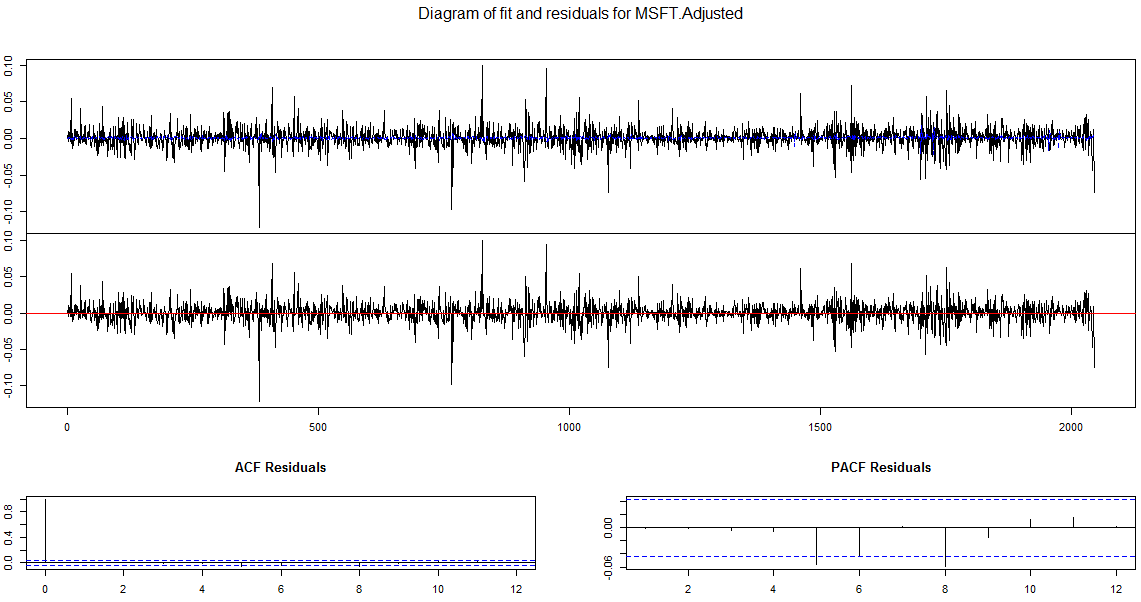

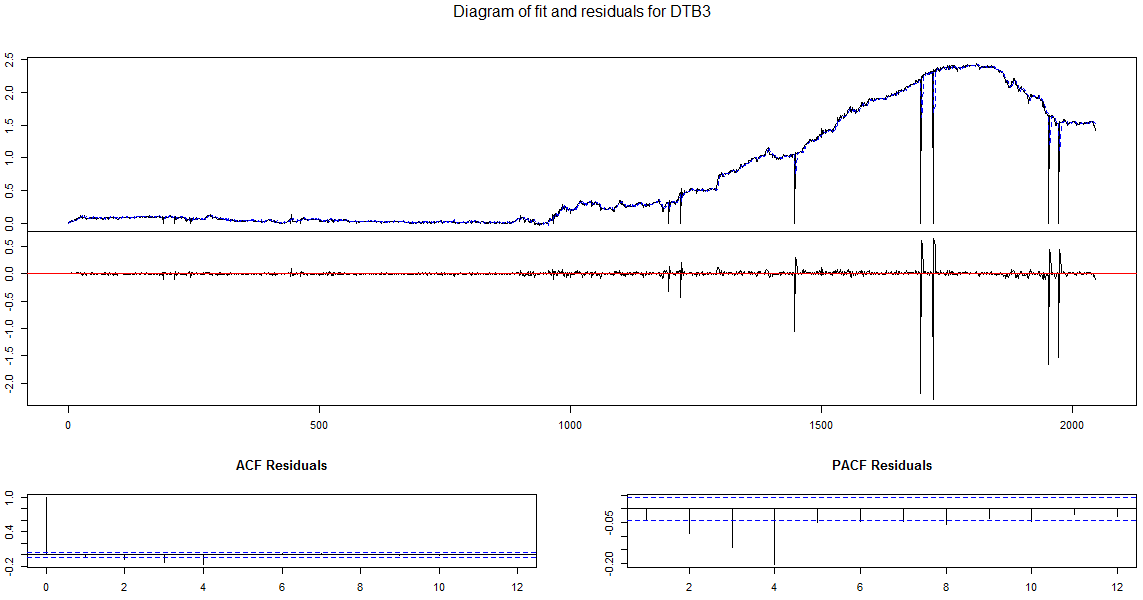

coef(var1) #concise summary of the estimated variables residuals(var1) #list of residuals (of the corresponding ~lm) fitted(var1) #list of fitted values Phi(var1) #coefficient matrices of VMA representation plot(var1, plot.type='multiple') #Diagram of fit and residuals for each variables

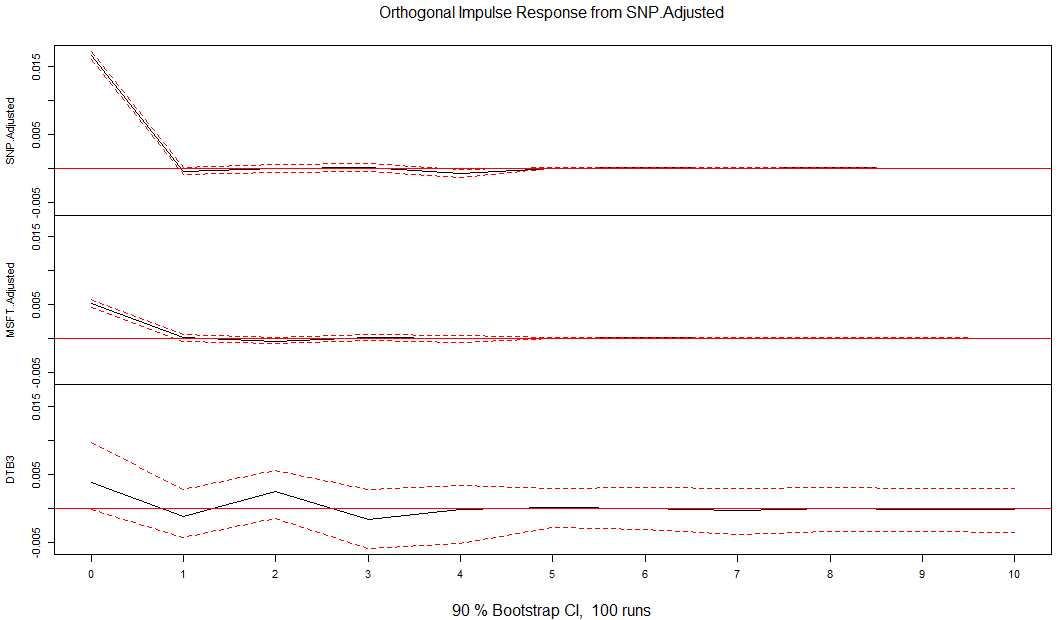

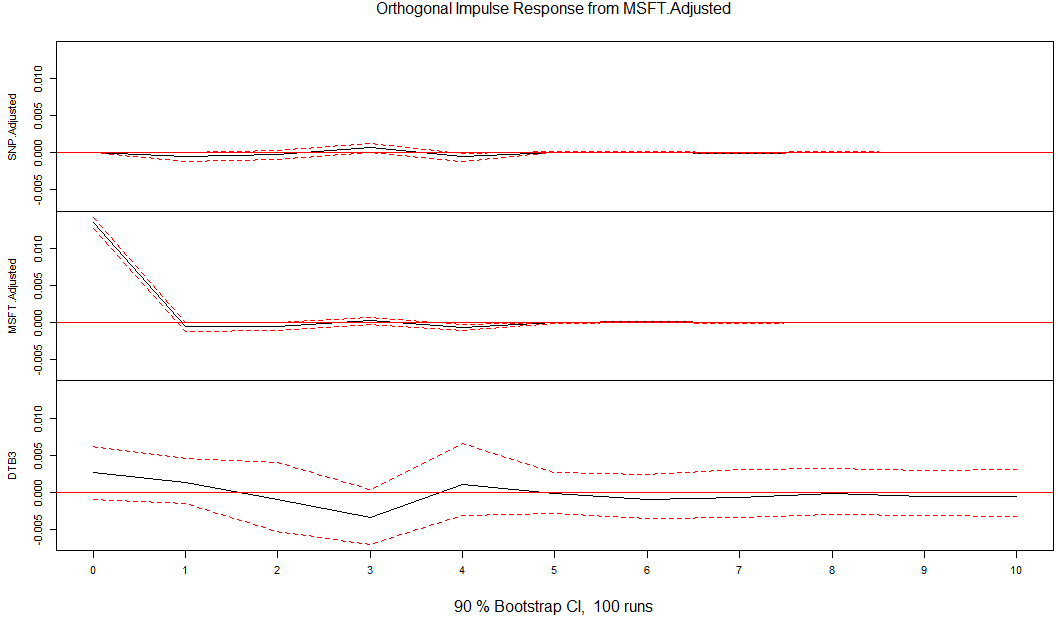

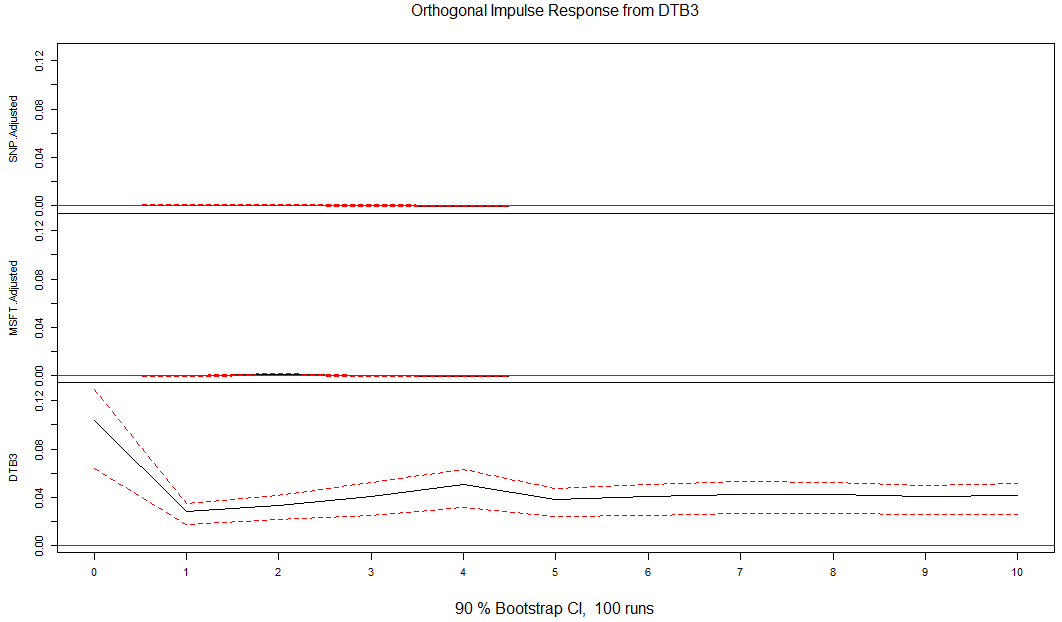

#confidence interval for bootstrapped error bands var.irf <- irf(var1, ci=0.9) plot(var.irf)

Number of required restrictions for SVAR model is K(K-1)/2, so in our case is 3.

浙公网安备 33010602011771号

浙公网安备 33010602011771号