【R语言学习笔记】9. 线性回归及其假设检验

1. 目的:构建线性回归模型并检验其假设是否成立。

2. 数据来源及背景

2.1 数据来源:数据为本人上课的案例数据,

2.2 数据背景:“玻璃制造公司”主要向新建筑承包商和汽车公司供应产品。该公司认为,他们的年销售额应与新建筑数量以及汽车生产高度相关,因此希望构建线性回归模型来预测其销售额。

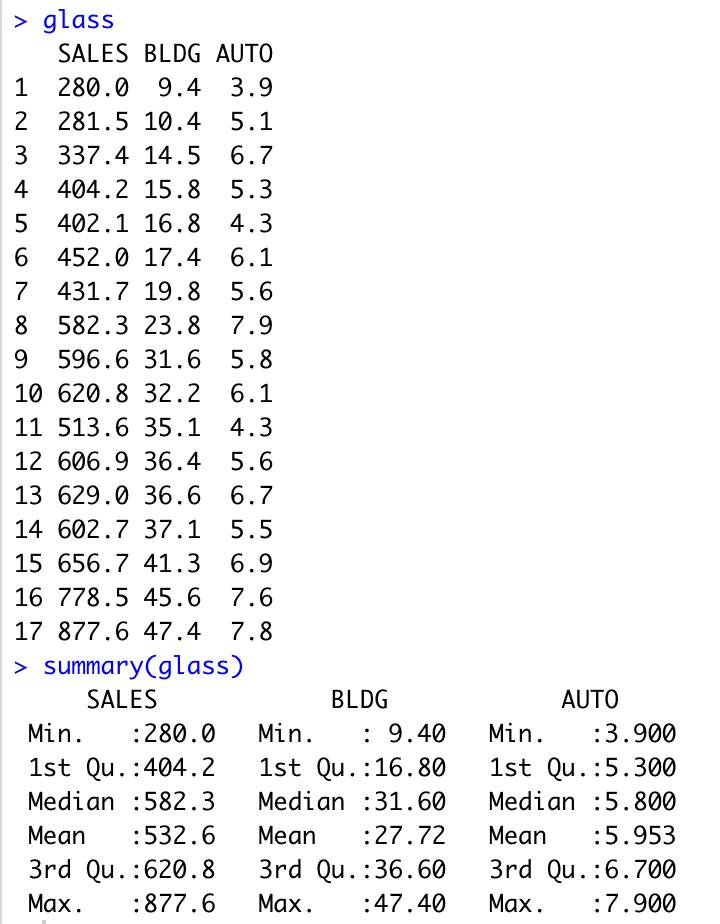

glass <- read.csv("glass_mult.csv",header=T)

glass

summary(glass)

3. 应用

3.1 模型构建

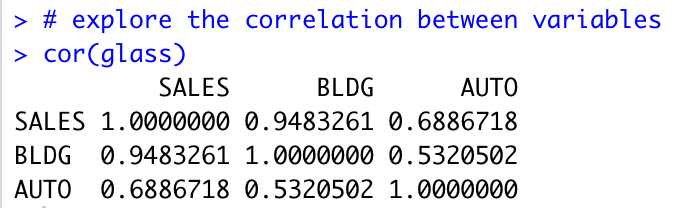

查看变量之间相关性,发现自变量BLDG与因变量SALES存在高达0.948的正相关性。

# explore the correlation between variables cor(glass)

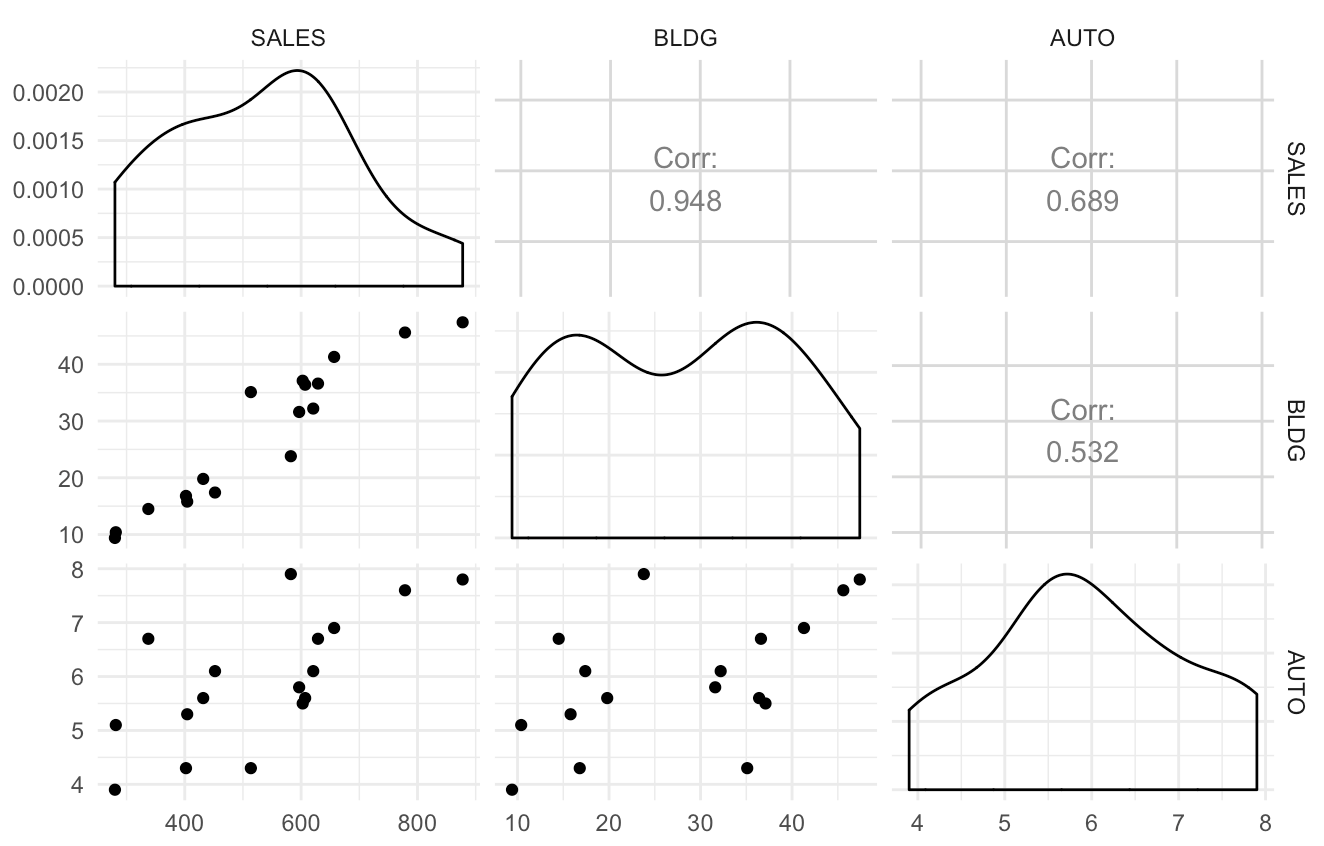

绘制任意两个变量之间散点图来探索其相关关系。

# get all scatter plots between 2 variables library(ggplot2) library(GGally) ggpairs(glass) ## alternative ## pairs( ~ SALES + BLDG + AUTO, data = glass)

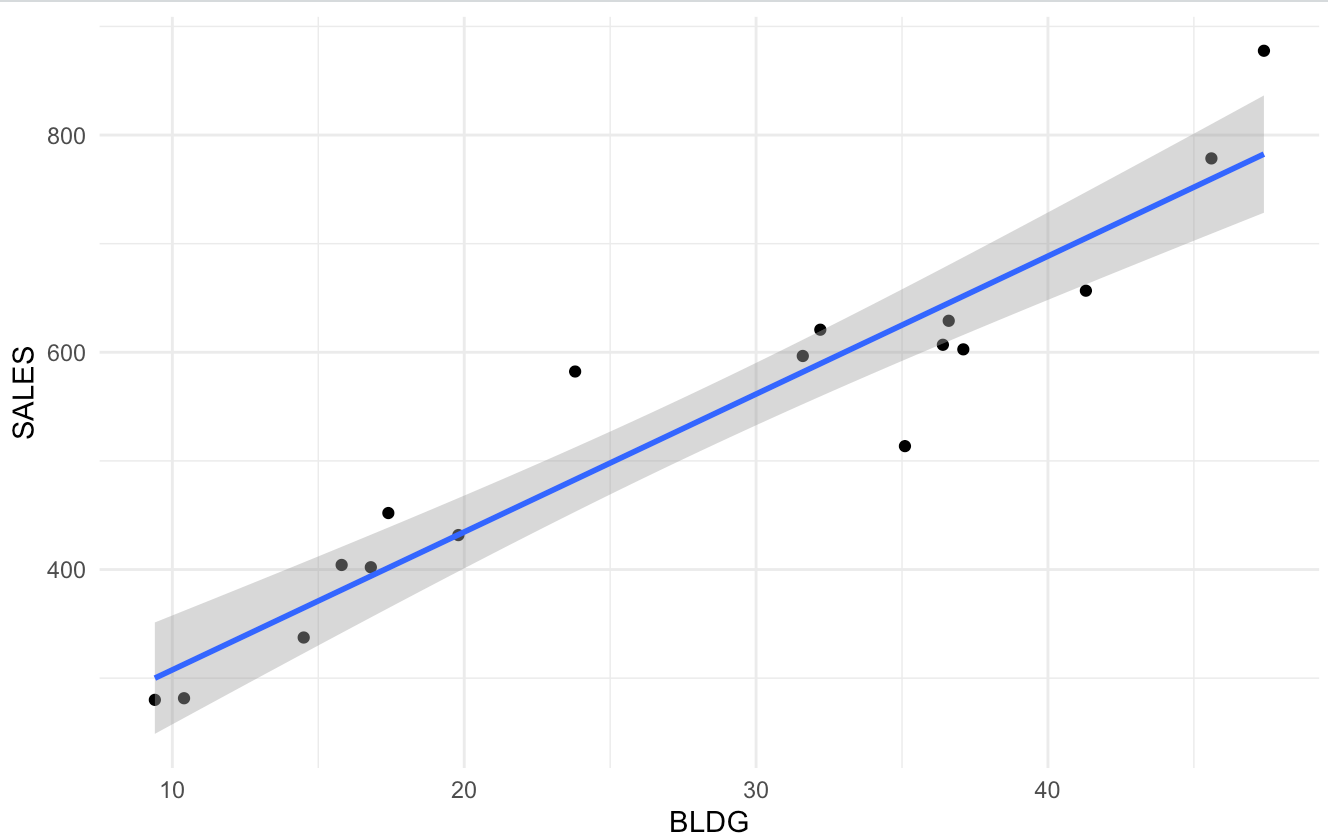

由于BLDG与SALES高度相关,故先构建二者之间的一元线性回归模型。

# build linear regression model 1 glass.lm1 <- lm(SALES ~ BLDG, data=glass) summary(glass.lm1) anova(glass.lm1)

根据模型结果,BLDG高度显著,且R-squared为0.8993,Adjusted R-squared为0.8926,说明该模型解释了将近90%的variance。

绘制BLDG与SALES的散点图,回归曲线,以及置信区间。

# plot the model as well as the real data

ggplot(glass, aes(x = BLDG, y = SALES)) + geom_point() + geom_smooth(method = 'lm')

# could add se = 'F' to geom_smooth to remove standard error lines

# alternative1

# ggplot(glass, aes(x = BLDG, y = SALES)) + geom_point() +

# geom_abline(intercept = coef(glass.lm1)[1], slope = coef(glass.lm1)[2])

# alternative2 ## plot(glass$BLDG, glass$SALES) ## abline(glass.lm1)

为了进一步理解一元线性回归模型,接下来手动构建一元线性回归模型并计算其参数(slope and intercept)。

# manually fit the simple linear regression model

library(dplyr)

glass %>%

summarise(

N = n(),

r = cor(SALES, BLDG),

mean_x = mean(BLDG),

sd_x = sd(BLDG),

mean_y = mean(SALES),

sd_y = sd(SALES),

slope = r * sd_y / sd_x,

intercept = mean_y - slope * mean_x

)

接下来,构建BLDG与AUTO的SALES模型。

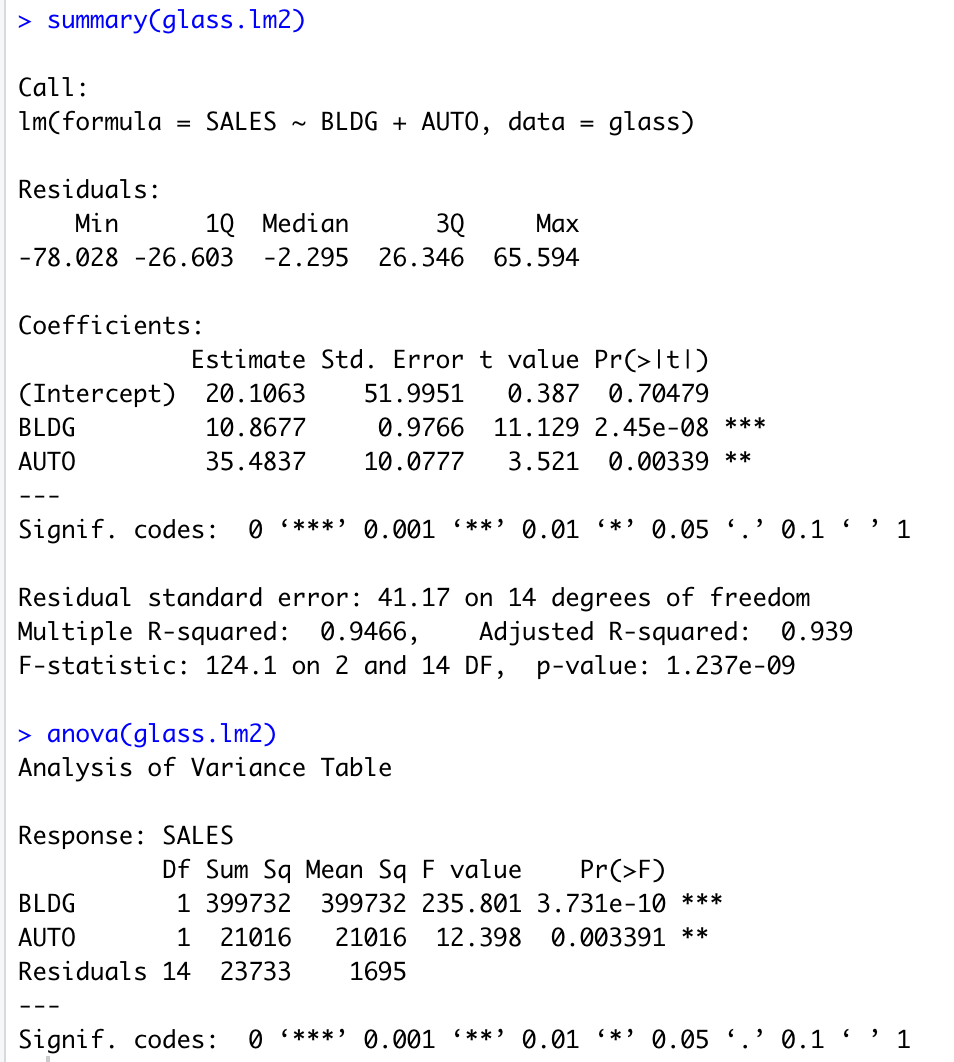

# build linear regression model 2 glass.lm2 <- lm(SALES ~ BLDG+AUTO, data=glass) summary(glass.lm2) anova(glass.lm2)

根据模型结果,两个自变量均高度显著,且R-squred及Adjusted R-squred分别提高至0.9446和0.939。

探索模型二是否在模型一的基础上具有显著的提升。由于P-value小于0.05,我们可以认为模型二与模型一相比有显著提升。

# check model improvement anova(glass.lm1, glass.lm2) # significant p-value means significant improvement

基于已有数据,运用模型二对其进行预测,并绘制真实值与预测值的散点图来观察预测准确性。

# model prediction glass$lm2.pred <- predict(glass.lm2) # compare the model prediction and the real data points ggplot(glass, aes(x = lm2.pred, y = SALES)) + geom_point() + geom_abline()

3.2 检验模型是否符合线性回归的假设

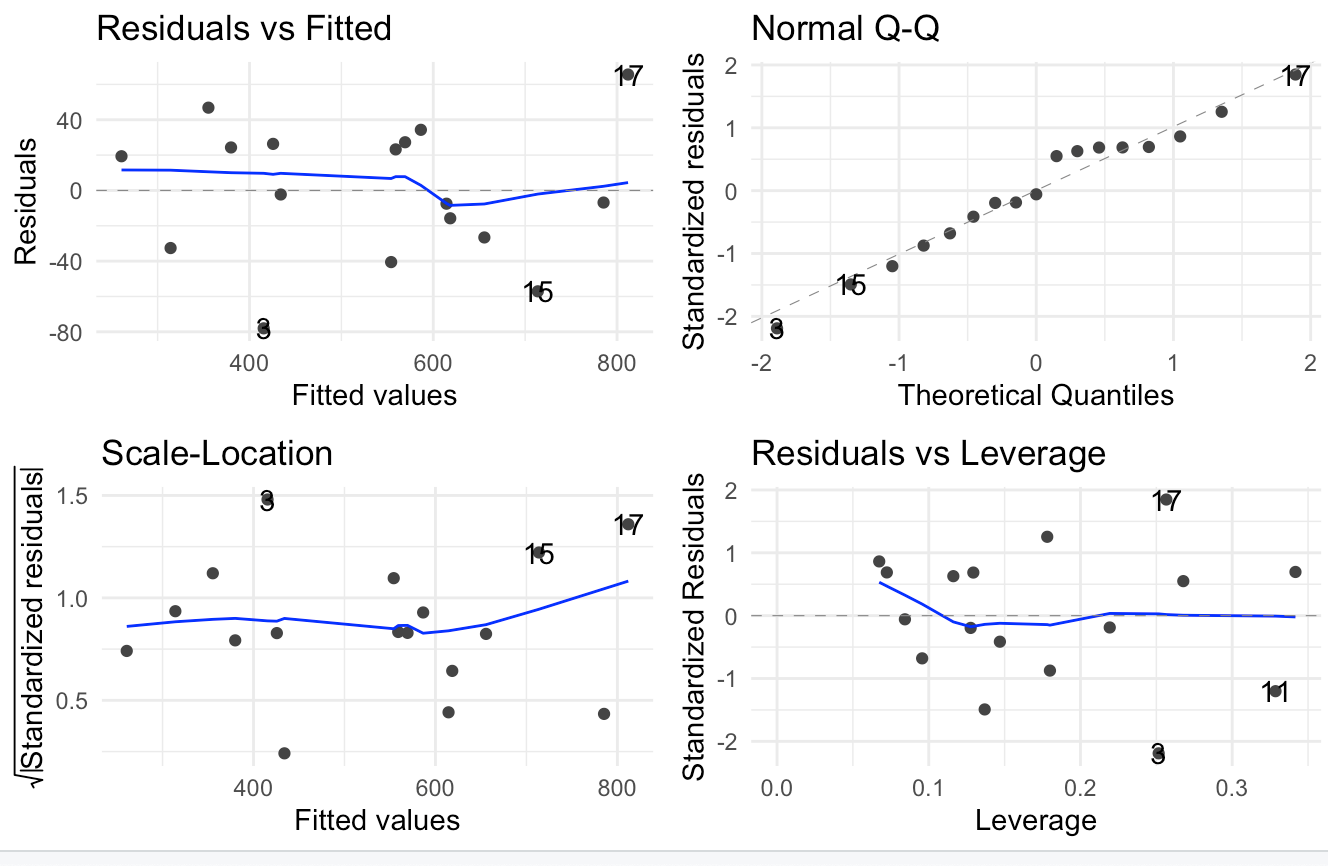

假设1: 自变量之间是独立的 (independence)

该假设可以通过3.1中探索变量之间的相关性来验证。若自变量之间的相关性小于0.7,则可认为符合假设。

假设2:自变量与因变量之间为线性/可加性的关系 (linearity)

该假设可以通过绘制散点图来判断

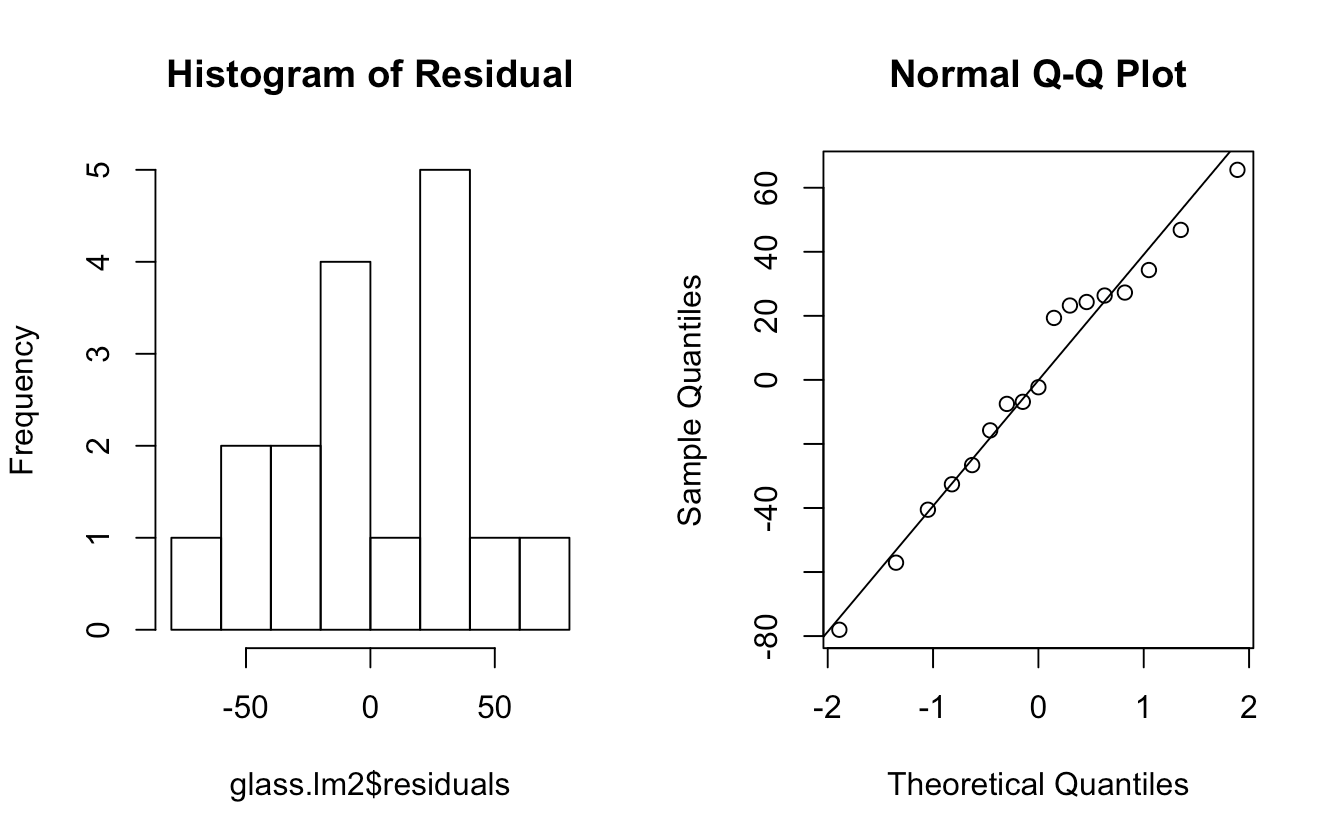

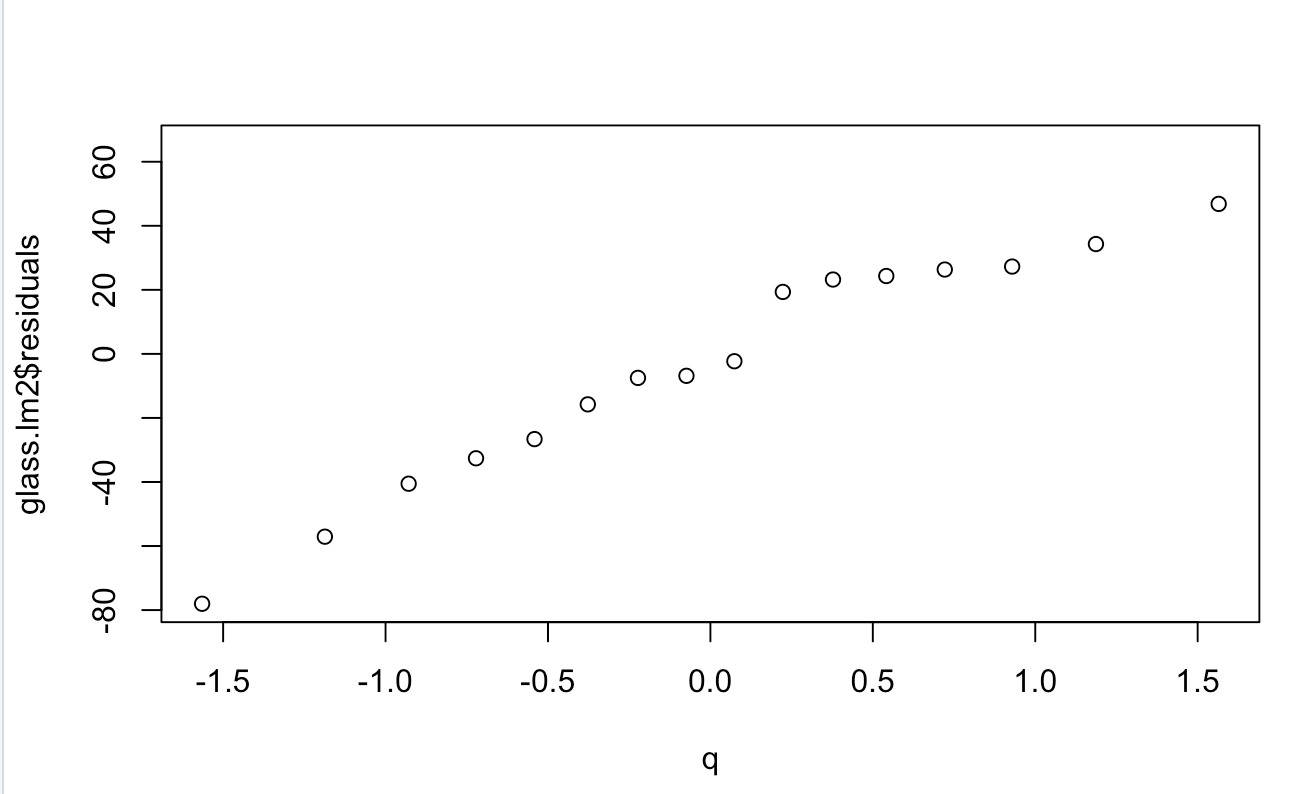

假设3:残差符合正态分布 (normality)

# test for normality

hist(glass.lm2$residuals, main = 'Histogram of Residual') qqnorm(glass.lm2$residuals) qqline(glass.lm2$residuals)

# alternative

## dat1 <- as.data.frame(glass.lm2$residuals)

## names(dat1) <- 'res'

## theme_set(

## theme_minimal() +

## theme(legend.position = "top"))

## ggplot(dat1,aes(sample = res)) + stat_qq()

# Shapiro–Wilk test # H0: 样本数据与正态分布没有显著区别。 # HA: 样本数据与正态分布存在显著区别。 shapiro.test(glass.lm2$residuals)

# roughly achieve qqplot by hand par(mfrow=c(1,1)) t <- rank(glass.lm2$residuals)/length(glass.lm2$residuals) #求观察累积概率 q <- qnorm(t) #用累积概率求分位数值 plot(q,glass.lm2$residuals)

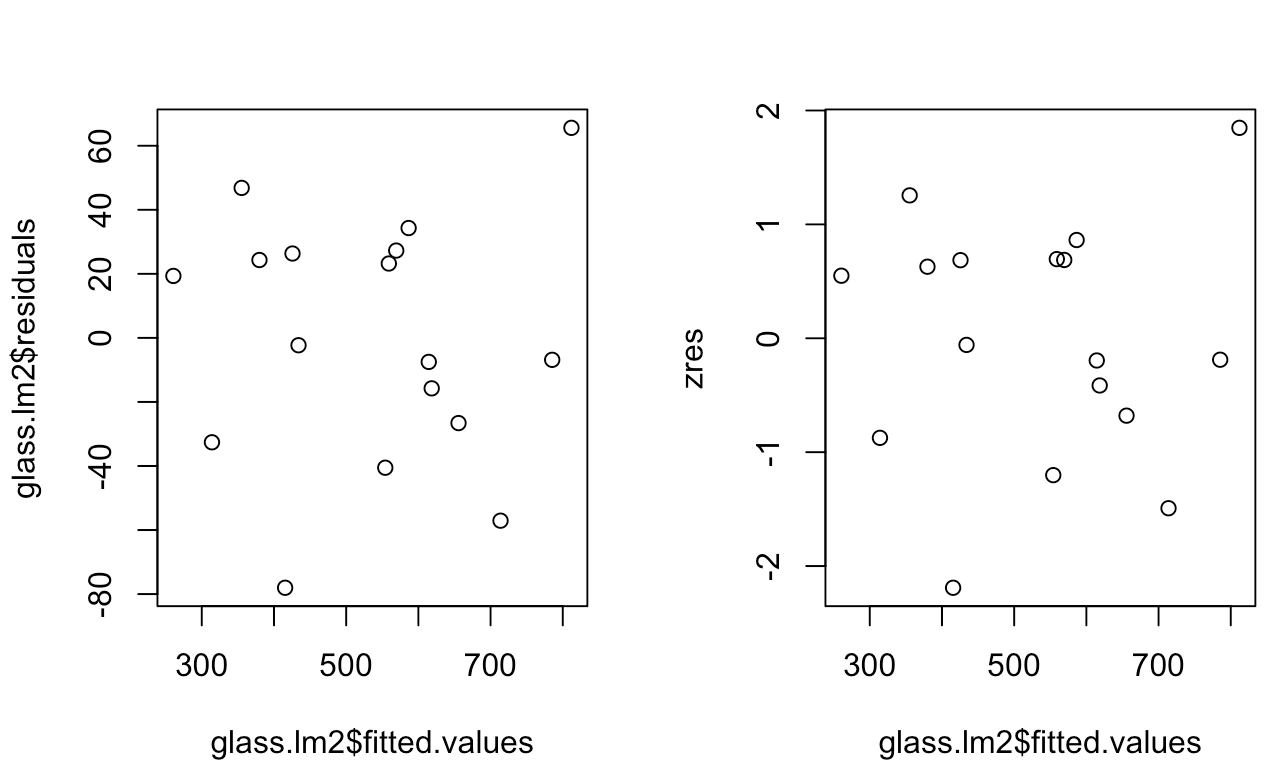

假设4:残差满足同方差性 (homoscedasticity)

# test for homoscedasticity par(mfrow=c(1,2)) plot(glass.lm2$fitted.values, glass.lm2$residuals) zres <- rstandard(glass.lm2) plot(glass.lm2$fitted.values, zres)

假设5: 残差满足独立性 (independence)

# test for independence par(mfrow=c(1,1)) data <- data.frame(YEAR=c(1:17)) newglassdata <- cbind(glass,data) #newglassdata plot(newglassdata$YEAR, glass.lm2$residuals)

# check model assumption in one step library(ggfortify) autoplot(glass.lm2) # alternative # par(mfrow = c(2,2)) # plot(glass.lm2)

浙公网安备 33010602011771号

浙公网安备 33010602011771号