python数学工具(一)

python 数学工具包括:

1.函数的逼近

1.1.回归

1.2.插值

2.凸优化

3.积分

4.符号数学

本文介绍函数的逼近的回归方法

1.作为基函数的单项式

对函数 ![]() 的拟合

的拟合

的拟合

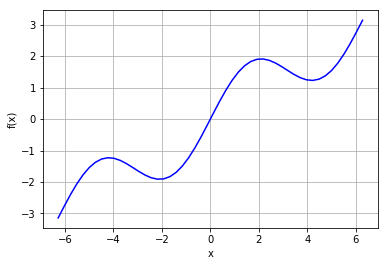

的拟合首先定义函数并且可视化

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

def f(x):

return np.sin(x)+0.5*x

x=np.linspace(-2*np.pi,2*np.pi,50)

plt.plot(x,f(x),'b')

plt.xlabel('x')

plt.ylabel('f(x)')

plt.grid(True)

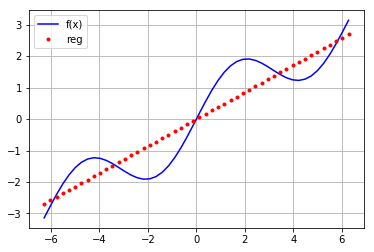

先用一次函数拟合

reg=np.polyfit(x,f(x),deg=1) ry=np.polyval(reg,x) plt.plot(x,f(x),'b',label='f(x)') plt.grid(True) plt.plot(x,ry,'r.',label='reg') plt.legend(loc=0)

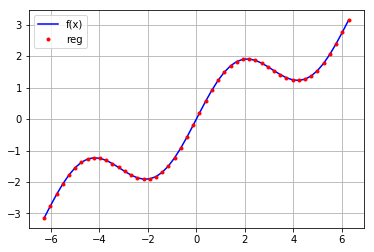

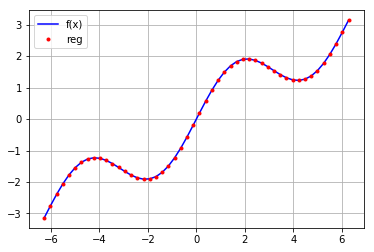

再用高次函数进行拟合

reg=np.polyfit(x,f(x),deg=16) ry=np.polyval(reg,x) plt.plot(x,f(x),'b',label='f(x)') plt.grid(True) plt.plot(x,ry,'r.',label='reg') plt.legend(loc=0)

拟合效果的检查

print('平均误差:',sum((ry-f(x))**2)/len(x))

平均误差: 3.16518401761e-13

np.allclose(ry,f(x)) True

2.单独的基函数

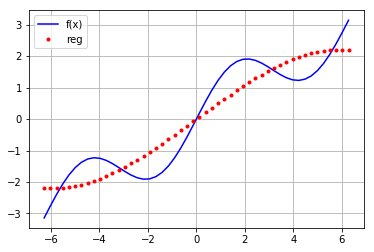

首先常见一个空的矩阵,然后为任一行添加函数

mat=np.zeros((3+1,len(x))) mat[3,:]=x**3 mat[2,:]=x**2 mat[1,:]=x mat[0,:]=1

reg=np.linalg.lstsq(mat.T,f(x))

#输出系数

reg[0]

array([ 1.52685368e-14, 5.62777448e-01, -1.11022302e-15,

-5.43553615e-03])

#输出图形 ry=np.dot(reg[0],mat) plt.plot(x,f(x),'b',label='f(x)') plt.plot(x,ry,'r.',label='reg') plt.grid(True) plt.legend(loc=0)

对每行的基函数进行变换:

mat=np.zeros((3+1,len(x))) mat[3,:]=np.sin(x) mat[2,:]=x**2 mat[1,:]=x mat[0,:]=1 reg=np.linalg.lstsq(mat.T,f(x)) ry=np.dot(reg[0],mat) plt.plot(x,f(x),'b',label='f(x)') plt.plot(x,ry,'r.',label='reg') plt.grid(True) plt.legend(loc=0)

3.多维情形

def fm(x,y):

return np.sin(x) + 0.25 * x + np.sqrt(y) + 0.05**y*2

x = np.linspace(0, 10, 20)

y = np.linspace(0, 10, 20)

x, y = np. meshgrid( x, y)

Z = fm(x,y)

x = x.flatten()

y = x. flatten()

import statsmodels.api as sm

matrix=np.zeros((len(x),6+1))

matrix[:,6] = np.sqrt(y)

matrix[:,5] = np.sin(x)

matrix[:,4] = y**2

matrix[:,3] = y**2

matrix[:,2] = y

matrix[:,1] = x

matrix[:,0] = 1

res=sm.OLS(fm(x,y),matrix).fit()

print(res.summary().as_text())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.999

Model: OLS Adj. R-squared: 0.999

Method: Least Squares F-statistic: 9.605e+04

Date: Tue, 31 Jul 2018 Prob (F-statistic): 0.00

Time: 10:51:36 Log-Likelihood: 661.47

No. Observations: 400 AIC: -1313.

Df Residuals: 395 BIC: -1293.

Df Model: 4

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 1.9548 0.010 193.732 0.000 1.935 1.975

x1 0.5891 0.005 111.546 0.000 0.579 0.600

x2 0.5891 0.005 111.546 0.000 0.579 0.600

x3 -0.0150 0.000 -54.014 0.000 -0.016 -0.014

x4 -0.0150 0.000 -54.014 0.000 -0.016 -0.014

x5 0.9533 0.004 251.168 0.000 0.946 0.961

x6 -1.6190 0.020 -79.979 0.000 -1.659 -1.579

==============================================================================

Omnibus: 4.352 Durbin-Watson: 0.880

Prob(Omnibus): 0.113 Jarque-Bera (JB): 4.214

Skew: -0.208 Prob(JB): 0.122

Kurtosis: 2.717 Cond. No. 4.93e+17

==============================================================================

浙公网安备 33010602011771号

浙公网安备 33010602011771号