The finnacial statements,taxes and cash flow

This chapter-2 we learn about the the financial statements(财务报表),taxes and cash flow.We must pay particular attention to two important differences:

1.the difference between accounting value and market value

2.the difference between accounting income and cash flow

Let's start:

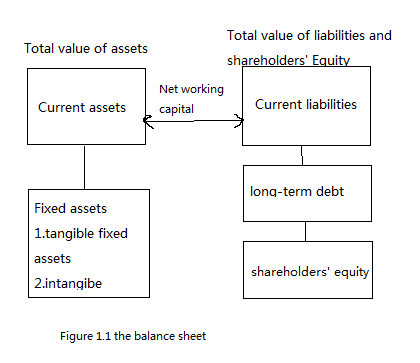

- 2-1 the balance sheet (资产负债表):it's a snapshot of a firm.Because it's a convenient means of organizing and summarizing what a firm owns(its assets资产),what a firm owes(its liabilities负债),and the difference between the two(the firm's equity股东权益) at a given piont in time.Now,let's take a look at the balance sheet:

1.Assets:the left-hand side

One thing we need to pay special attention is about current assets:A current asset has life of less than one year.This means that the asset will normally convert to cash within 12 month,for example,inventory,cash,accounting receivable(money owed to the firm by it customers)...

2.Liabilities and Owners' equity:the right-hand side

Like the current asset,current liabilities have a life of less than one year(meaning they must be paid within a year),accounting payable(money the firm owes to suppliers)...Like the load,it's a long-term debt.Firm borrow over the long term from a variety of sources.We tend to use the terms bonds and bondholders(generically to refer to long-term debt and long-term creditors,respectively)

3.The balance sheet identity or equation:assets = liabilities + shareholders' equity (left = right),Shareholders' equity is defined as the difference between assets and liabilities.

4.Net working Capital:净营运资本 = current assets - current liabilities

Net working capital is positive when current assets exceed current liabilities.(In a healthy firm)

5.There are three particularly important things to keep in mind when examining a balance sheet:

1)Liquidity(流动性):the speed and ease(容易程度) with which an asset can be converted to cash.Gold is relatively liquid asset,but a custom manufacturing facility is not.Liquidity really has two dimensions:ease of conversion versus loss of value.Any asset can be converted to cash quickly if we cut the prrice enough.A highly liquid asset is therefore one that can be quickly sold without significant loss of value.An unliquid asset is one that cannot be quickly converted to cash without a substantial price reduction.

Assets are normally listed on the balance sheet in order of decreasing liquidity.Current assets are relatively liquid and include cash and those assets that we expect to convert to cash over the next 12 months.But fixed assets are,for most of part,relatively illiquid.

Liquidity is valuable.The more liquid a business is, the less likely it is to experience financial distress(that is ,diffculty in paying debts or buying needed assets).Unfortunately,liquid assets are generally less profitable to hold.For example,cash holding are the most liquid of all investments,but they sometimes earn no return at all--they just sit there.There is therefore a trade-off between the advantages of liquidity and forgone potential profits.

2)Debt versus Equity(负债和权益):Equity holders are only entitled to the residual value.(Shareholders' equity = assets -liabilities)

The use of debt in a firm's capital structure is call financial leverage.The more debt a firm has,the greateer is its degree of financial financial leverage.Debt acts like a lever in the sense that using it can greatly magnify both gains and losses.So,financial leverage increases the potential reward to shareholders,but it also increases the potential for financial distress and business failure.

3)Market value versus Book value(市场价值和账面价值):The true value of any asset is its market value,not the value shown on the balance sheet(Book value).According to GAAP(Generally accepted accounting principles,公认会计准则),financial statements show at history cost.In other words,assets are "carried on the books" at what the firm paid fir them, no matter how long ago they were peuchased or how much they are worth today.

Managers and investor will frequently be interested in knowing the market value of the firm.This information is not on the balance sheet.The fact that balance sheet assets are listed at cost means that there is no necessary connection between the total assets shown and the market value of the firm.Indeed,many of the most of valuable assets that a firm might have---good management,a good reputation,talented employees---don't appear on the balance sheet at all.Thus,we all concern about the maeket value but not the book value on the balance sheet.

'cause there are too many contents in this chapter,so in next section we will continue to talk something about "the income statement"(损益表),welcome to focus again!